.jpeg)

Global Student Flows | Canada

3 November 2025

This report takes a wide-angle view of Canada’s international student mobility. Using an evidence-based framework, we model possible futures for student recruitment through 2030 under three scenarios: Regulated Regionalism, Hybrid Multiversity, and Talent Race Rebound. These scenarios provide higher education leaders with the foresight needed to plan strategically for the decade ahead.

Read a snippet below, or download the PDF to access all the insights.

Overall, we forecast the number of international students in Canada to drop steeply in 2025 and 2026, but recover as we move towards 2030, resulting in an average annual contraction of 1%. This contraction is primarily due to the Canadian government implementing a cap on international students, down to 437,000 in 2025 from over 650,000 in 2023.

After a growth period post-COVID, Canadian institutions will be forced into a battle for market share. No longer able to rely on rapid expansion, Canadian institutions must differentiate their offering – whether by aligning curricula to employer needs, increasing reputation or offering innovative delivery models, such as world-class online programs.

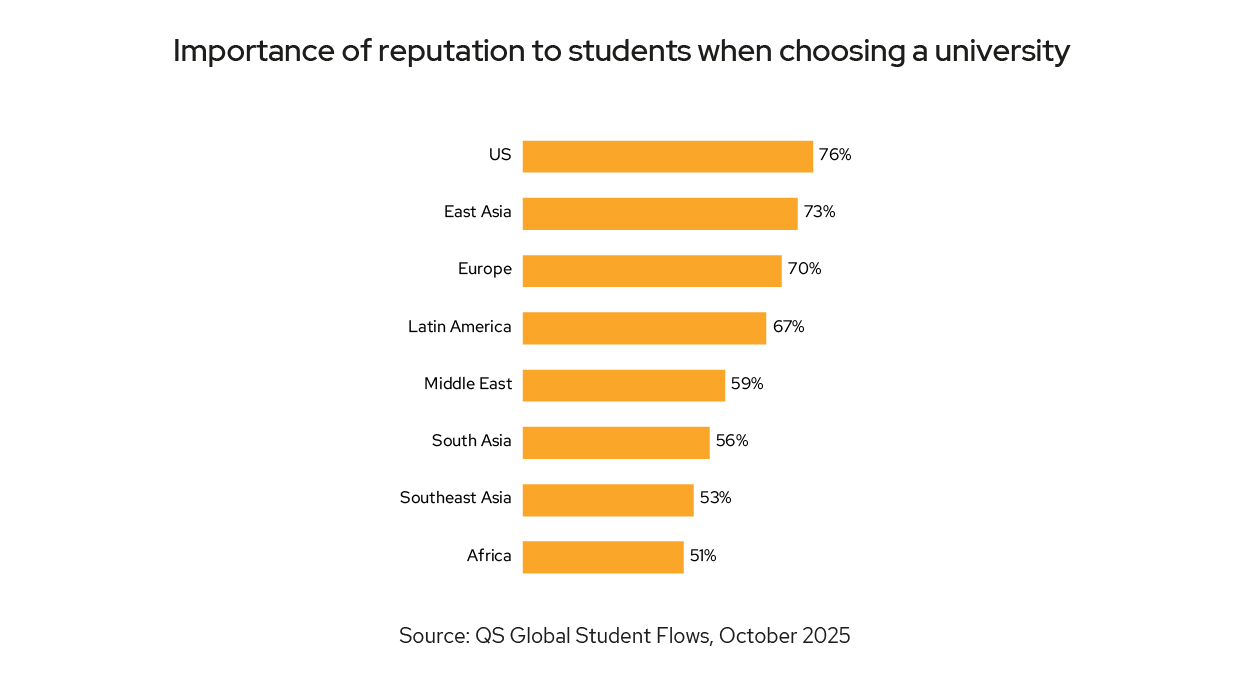

Understanding your target markets is crucial for institutions looking to increase enrollments in a low-growth environment. QS International Student Survey data shows students consider reputation when making study decisions.

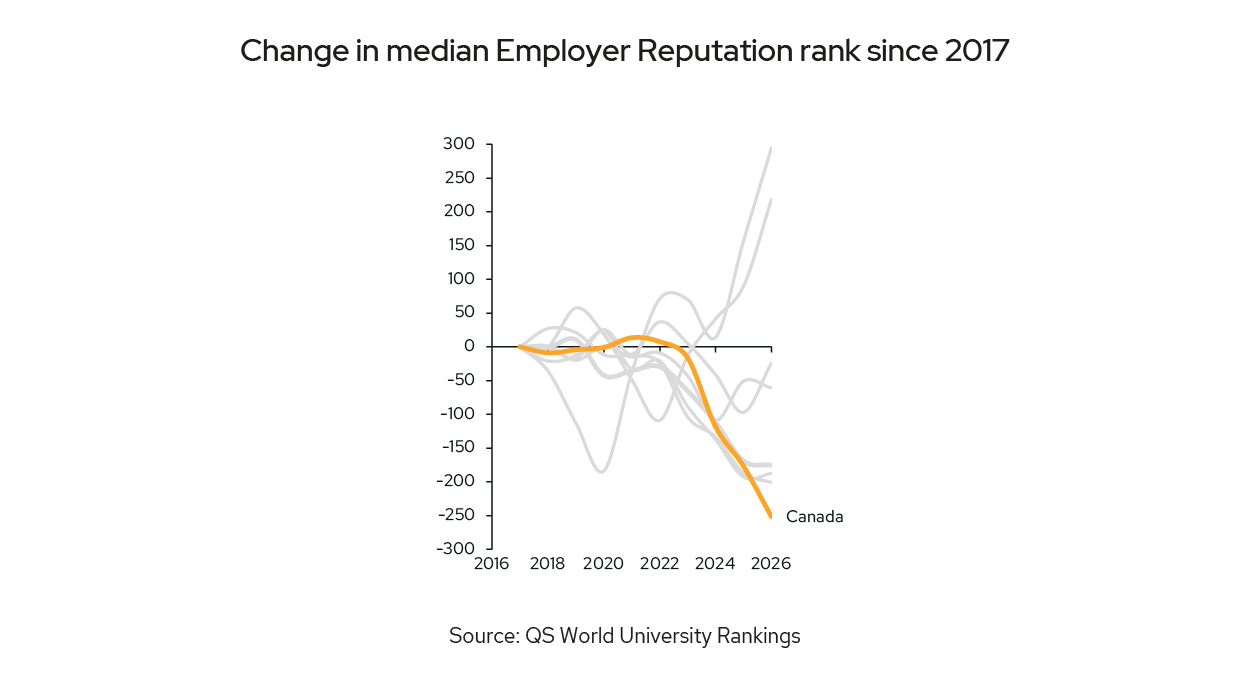

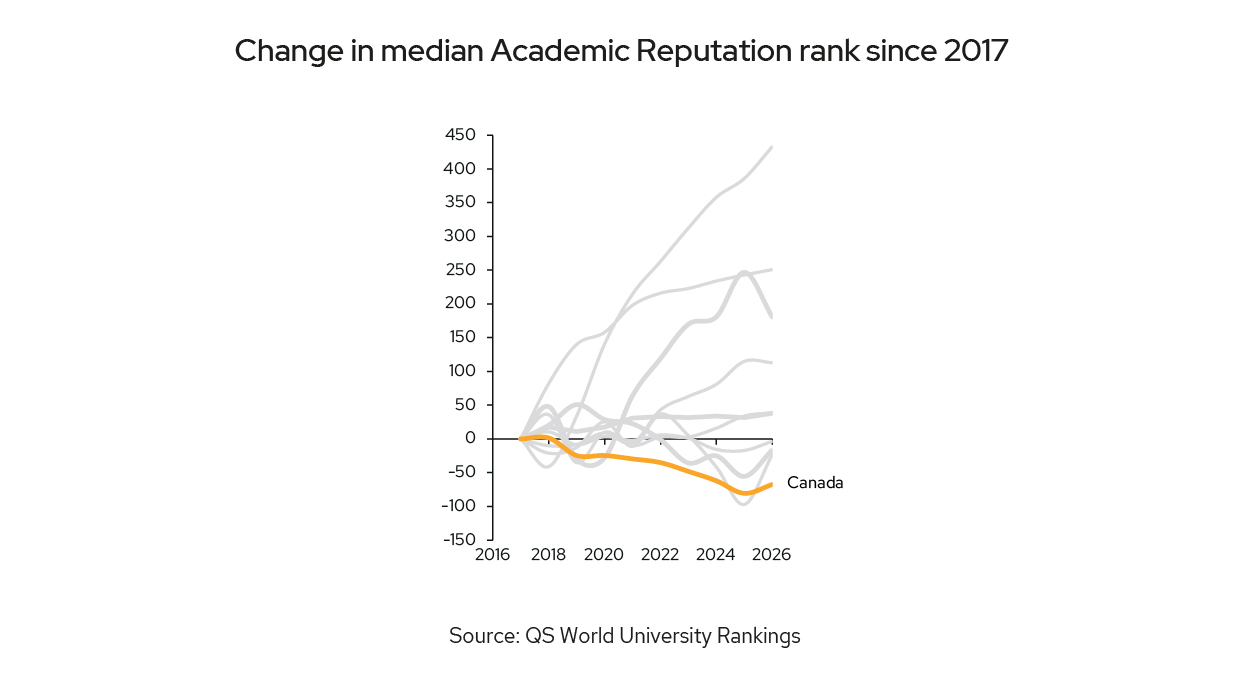

The median Academic and Employer Reputation rank of Canadian institutions has seen a dramatic decline since 2017. At the same time, the importance of reputation to prospective students has increased, and other countries, such as Malaysia, have rapidly improved their reputation performance. At a time of low growth, Canadian institutions need to rebuild their reputation among key stakeholder groups, or students may look to study in other countries that are both closer to home, and lower in cost.

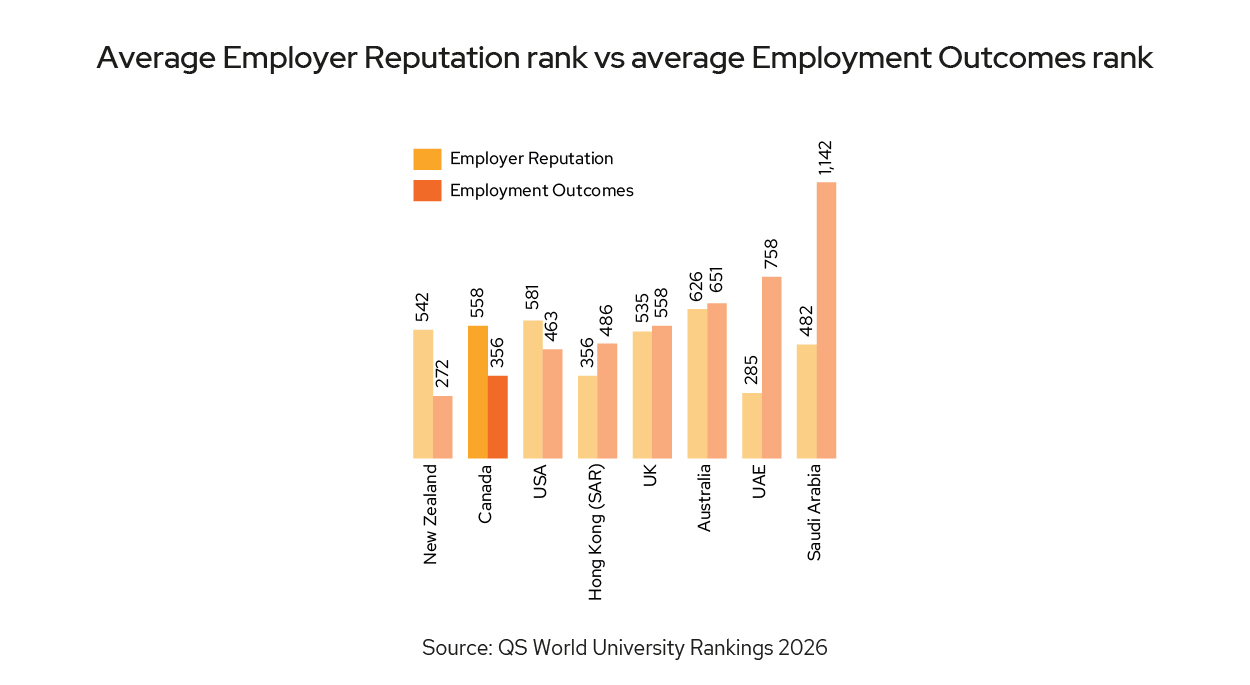

For students looking to study in Canada, post-graduate employment, skills development and return on investment are key priorities. Fortunately, our Employment Outcomes metric shows Canadian institutions are performing well. However, this is not translating into a strong Employer Reputation. Canadian institutions need to ensure that their students are graduating with the skills that employers require by aligning curricula to business needs, bolstering careers services, and embedding experiential, work-based learning across programs.

Amid uncertain policy environments, it’s critical that institutions do not commit to a single plan, and instead integrate flexible, scenario-based planning. Our three scenarios, Regulated Regionalism, Hybrid Multiversity, and Talent Race Rebound offer three potential futures to help guide leaders’ decision-making.

1. Increasing Competition Threatens Institutions’ Financial Stability

Following a period of growth, institutions must now adapt to a lower growth environment. What can institutions do to mitigate the impact of decreasing student numbers?

2. Labor Market AlignmentIncreasingly, students look for data and information about the return on their investment, and what career they will be able to have because of their degree. How are institutions articulating their employability expertise during the student recruitment process?

3. Emerging International Education Hubs Outside the ‘Big Four’

The growing attractiveness of destinations in Asia and the Middle East could present new competition in an already challenging recruitment market. How can Canadian institutions compete against lower-cost alternatives that are rapidly improving their reputation?

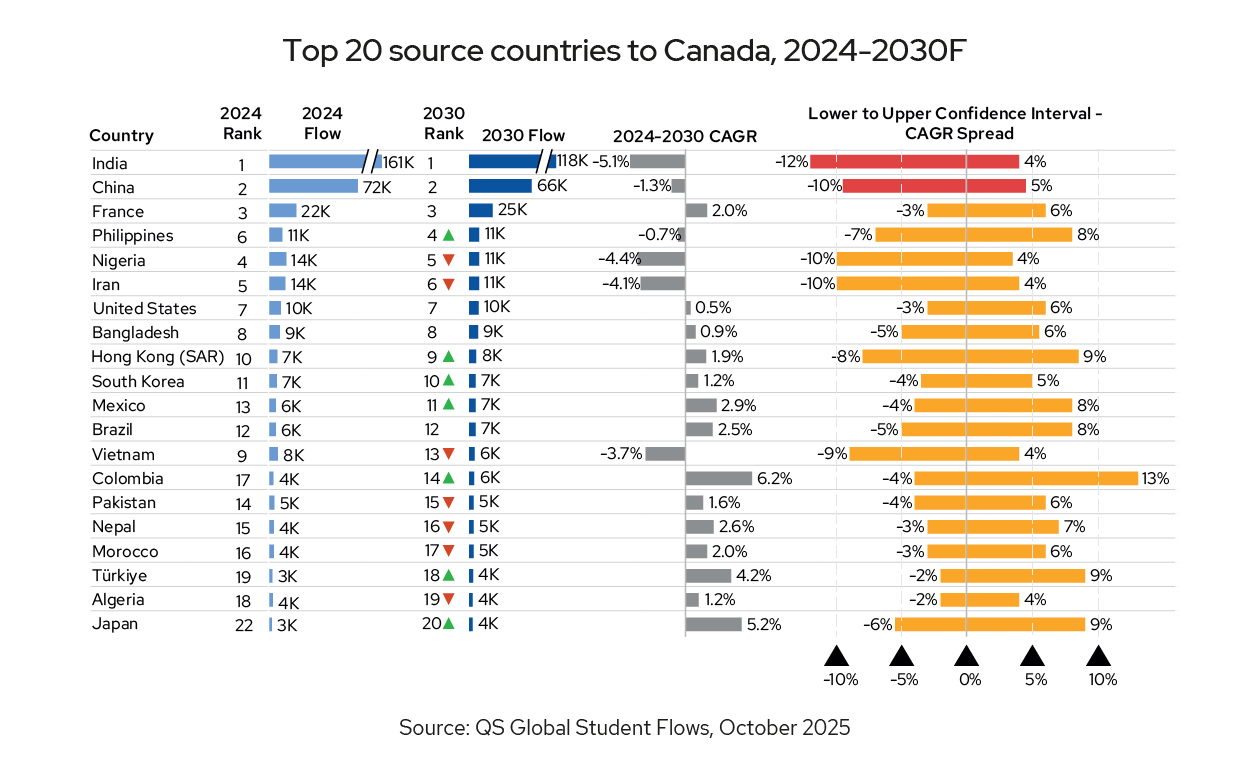

Canada’s international education sector is in the midst of its most significant adjustment in two decades. After years of unrelenting growth, the country’s foreign student inflows have entered a sharp correction phase — triggered first by federal policy caps and then compounded by growing perception challenges abroad. Yet while 2024—2026 marks a clear downshift, the story through 2030 may not be one of steady decline. Rather, we predict it could be one of contraction, recalibration, and eventual stabilization toward the end of the decade.

In early 2024, Canada introduced an intake cap aimed at reducing new study permits by roughly 40% — a move designed to cool overheated housing markets and address concerns about the integrity of parts of the international education system. In 2025, the federal government reduced approved study permits by a further 10%. The adjustment had an immediate impact; by 2025, several large universities and colleges were reporting 40–50% declines in new foreign student enrollments compared with the previous year.

Given these developments, we estimate that the stock of international students enrolled in Canadian institutions will decline by around 10% in 2025 and 2026 with an eventual stabilization expected towards the end of the decade. Over the full 2024–2030 period, this translates into an average annual contraction of roughly 1%, following years of double-digit growth. The projected 1% annual decline would reduce international post-secondary enrollments from about 470,000 in 2023 to 415,000 by 2030*.

The adjustment follows an extraordinary decade of expansion. Between 2012 and 2023, Canada’s international student population more than tripled, propelled by aggressive recruitment in India, China, and Francophone Africa. Universities, colleges, and private institutions alike grew reliant on foreign enrollments and that dependence has now become a source of vulnerability. With inflows falling, institutions face budget squeezes, deferred projects, and hiring freezes. In a sector where foreign students also cross-subsidize domestic enrollments, this contraction risks cascading effects across teaching quality, research activity, and even local economies reliant on student spending.

Even before the announcement of the cap, there were early signs of fatigue in key sending markets. Rising costs of living, visa delays, and housing shortages had begun to tarnish Canada’s image as an accessible and student-friendly destination. In India, by far Canada’s largest source market, a perception shift due to uncertainty and a pivot toward alternative destinations such as the UK and Australia is expected to result in a significant drop in student numbers – from 160,000 to 120,000 by 2030. In China, where outbound mobility has only partially recovered after the pandemic, Canada’s recent policy volatility has further cooled demand. Meanwhile, emerging markets in Southeast Asia and Latin America — previously seen as diversification opportunities — are unlikely to compensate for the shortfall in the short term.

Yet the outlook is not uniformly grim. Our projections suggest the sharpest declines will be concentrated in 2024–2026, followed by a gradual stabilization and mild recovery toward the late 2020s. This turnaround is not driven by optimism, but by structural realities, as the system is not likely to be able to sustain a prolonged contraction of this scale.

A steep, sustained drop in student numbers would create collateral challenges — from shortages in critical skill pipelines (notably in healthcare, technology, and engineering) to the financial strain on public universities that underpin regional economies. Historically, major destination countries that have experienced similar downturns (such as Australia in the early 2010s) have seen a rebound once policy uncertainty eased and recruitment efforts recalibrated.

Our baseline forecast therefore assumes that from 2027 onward, new inflows begin to recover modestly, leading to slow but positive growth in total international enrollments by 2029–2030 — an annual rate of around 5%.

For stakeholders, the key takeaway from this forecast is not just the headline decline but the uncertainty that surrounds it. While current indicators suggest a contraction through 2026, it would be a mistake to plan exclusively for prolonged pessimism. Historically, the international education market has shown remarkable elasticity; sharp declines often give way to rebounds as policy clarity and global demand return. Our inclusion of a late-decade recovery is not a prediction of inevitability, but a recognition of prudent foresight in uncertain times. In highly uncertain environments, institutions are better served by flexible, scenario-based planning rather than committing to a single trajectory that may be distorted by short-term sentiment.

By 2030, Canada’s international education landscape will look different from the pre-2024 era. The period of runaway expansion is over; a more measured, strategically focused phase is emerging. Student numbers may be lower than their 2023 peak, but the sector could emerge leaner, more diversified, and more resilient. In the best-case scenario, Canada will have rebuilt confidence abroad, restored a sustainable inflow of high-quality students, and strengthened its reputation for academic excellence. In the worst-case scenario, policy drift and perception issues could see its global market share erode permanently to competitors. Either way, the next few years will be decisive for universities, policymakers, and investors alike.

*Our base figures differ from the widely cited one million international students as that total includes all study permit holders, not just those enrolled in higher education. Our figures also focus solely on postsecondary enrollments. The distinction matters as the gap between study permit holders and actual enrollments is substantial at the post-secondary level.

and How They Impact Canada

Regulated Regionalism reflects a scenario in which Canada’s international higher education system is reshaped by government-led policies to create a more regionally balanced model aligned with national and local capacities. In this model, following years of rapid growth, the federal government introduces structured controls, most notably the national study permit cap, which allocates limits to provinces and territories based on housing availability, institutional capacity, and labor market priorities.

The National Study Permit Cap, a federally imposed hard ceiling on new international student arrivals, is not applied uniformly but is distributed among the provinces and territories based on population, resulting in significant regional variance. The system explicitly links intake to local capacity, allowing provinces outside major cities to use their allocations to support regional immigration and drive economic growth in less-populated areas.

Canada has also replaced the broad link between study and permanent residency with a selective system focused on retaining high-skilled workers. Access to a post-graduation work permit (PGWP) is now tightly limited: non-degree graduates qualify only in shortage fields such as trades, health, or STEM, and must meet new language requirements. Graduates of public-private partnership colleges have lost PGWP eligibility entirely. In contrast, master’s and doctoral graduates receive extended PGWPs, with spousal work rights reserved — shifting immigration benefits toward highly educated, research-focused talent. Regulated Regionalism.

These measures, alongside higher financial requirements, make studying in Canada costlier and less accessible, redirecting demand toward regional and domestic alternatives. Students from South Asia, West Asia, and Sub-Saharan Africa are increasingly choosing local or nearby options, as countries like India, the UAE, Malaysia, and Saudi Arabia expand their higher education systems and transnational partnerships. This emerging, distributed model reduces costs and distances for students while easing housing and service pressures in Canada’s major cities. It also channels a smaller, more strategically valuable intake toward regions and programs aligned with labor shortages and immigration goals. Under Regulated Regionalism, Canada would need to focus on quality and capacity over growth

Hybrid Multiversity describes the strategic shift of Canada’s international education system, driven by the National Study Permit Cap and high living costs that limit the number of students physically present in Canada. The model allows Canadian institutions to sustain enrollments, quality, and revenue through coordinated, multi-site structures that blend online, regional, and short, high-impact in-country learning.

Many international students complete a substantial portion of their degree online or through regional arrangements, such as Transnational Education (TNE) partnerships or international branch campuses. Their time in Canada is limited to shorter, structured periods that focus on high-value, hands-on experiences that cannot be replicated remotely. These include co-op placements and internships that provide Canadian workplace experience, specialized laboratory and clinical training, fieldwork, and intensive professional networking opportunities. This approach ensures that students gain the practical skills and local exposure necessary for integration into the Canadian labor market while minimizing the constraints of limited campus capacity and high living costs.

Institutions implement shared credit-transfer systems and common quality standards across partnerships to ensure academic quality and mobility. Faculties align curricula and assessments so that degrees partly earned abroad meet Canadian standards. Canadian campuses are repositioned as specialized hubs, emphasizing infrastructure and workplace-integrated learning critical for PGWP eligibility.

Career development is embedded throughout. Micro-credentials earned remotely are integrated into transcripts, giving employers early visibility of student skills. Short-term remote internships lead to mandatory in-Canada placements aligned with regional labor needs. For this model to succeed, Immigration, Refugees and Citizenship Canada (IRCC) must introduce flexible, short-term visa pathways and ensure PGWP rules recognize online and TNE components.

Hybrid Multiversity offers a sustainable, flexible, and distributed approach to international education. It expands Canada’s global reach and revenue potential without straining local housing or services, while linking in-country experiences to strategic employment opportunities, affordability, and long-term access to global talent.

Talent Race Rebound describes a future in which the ‘Big Four’ reverse the restrictive international education policies of the mid-2020s and position global student recruitment as a central strategy to address workforce shortages and demographic challenges. By 2030, the focus shifts from limiting enrollment to actively expanding intake in high-demand, high-skill sectors such as artificial intelligence, quantum technology, biotech, advanced manufacturing, and healthcare.

The temporary study permit caps and bureaucratic delays of 2024—2025 are replaced by streamlined, student-focused processes that provide certainty and speed for applicants. PGWPs are extended and targeted to priority STEM and health disciplines, and these credentials are explicitly recognized within Express Entry and Provincial Nominee Programs, creating a clear pathway to permanent residency. Universities and colleges operate in close coordination with federal and provincial governments, as well as industry partners, to align curricula and internships with labor market needs. National scholarship programs are significantly expanded to attract students in priority fields, while private-sector co-investment supports graduate internships and guarantees employment outcomes for high-performing international graduates. Multi-year public research grants and major infrastructure investments, including dedicated AI and biotech centers, strengthen Canada’s ability to compete globally for top faculty and students.

Universities and colleges operate in close coordination with federal and provincial governments, as well as industry partners, to align curricula and internships with labor market needs. National scholarship programs are significantly expanded to attract students in priority fields, while private-sector co-investment supports graduate internships and guarantees employment outcomes for high-performing international graduates. Multi-year public research grants and major infrastructure investments, including dedicated AI and biotech centers, strengthen Canada’s ability to compete globally for top faculty and students.

Infrastructure constraints, particularly housing shortages that previously limited student intake, are addressed through national and provincial investment strategies, including large-scale public-private partnerships focused on student housing and mixed-use developments in regional cities and smaller urban centers. This approach allows for greater enrollment while distributing international talent more evenly across the country, easing pressure on major metropolitan areas such as Toronto and Vancouver.

For students from emerging markets like India, Nigeria, and Brazil, Canada becomes highly attractive. The country offers a full on-campus experience, access to world-class academic and research environments, integrated professional networks, and a clear, fast-tracked pathway to employment and permanent residency. International education is no longer primarily a source of operational revenue but a strategic tool in Canada’s national competition for the skilled talent necessary to sustain economic growth and address demographic challenges.

This scenario represents a decisive pivot from restriction to opportunity, demonstrating how targeted policy, investment, and institutional coordination can transform international education into a core lever for national development.

For students looking to study in Canada, reputation is an increasingly important factor. In Canada’s second largest source market – East Asia – nearly 75% of students say reputation is important when deciding which university to study at. In all markets, 60% of students say reputation is important.

However, the median Academic and Employer Reputation rank of Canadian institutions has seen a significant decline since 2017, making overall reputation a real risk factor for institutions looking to increase inbound student flows.

While fellow Big Four countries have seen declines, other nations have seen their reputation rapidly grow, and now threaten the hegemony of the Big Four. While these countries – such as the UAE, Saudi Arabia, and Malaysia – currently face constraints around capacity, infrastructure, and proven career outcomes, they still pose a future risk to Canadian flows, should they solve these problems.

It’s vital that institutions have the necessary regulatory support to maintain their global status, as their reputation has seen a significant decline in the last 10 years. Rebuilding reputation should be a key pillar of institutional strategy, as it will enable Canadian universities to harness international student flows from the US, Europe, and East Asia – crucial source markets for future growth.

Additionally, students draw an implicit association between reputation and ranking performance: 71% of students say that good performance in rankings is indicative of a good reputation. This is compounded by the fact that only 12% of students looking at Canada will prioritize an institution’s rank without also prioritizing reputation. Ranking performance is also one of the most important factors to students when gauging teaching quality at an institution, cited by 60% of students.

Post-study employment prospects are a vital consideration for most students. Nearly half of all students looking to study in Canada say that information on work placements and links to industry are key topics they want to hear about in marketing materials.

Regardless of region, a majority of students say that when thinking about career considerations while choosing a course, they base their decision on whether the program allows them to learn new skills. Evidently, students view their time at university as the ideal opportunity to upskill and to learn how to articulate the value they can add to prospective employers through the skills they acquire.

This eagerness should help solve another issue facing Canadian institutions: the dissonance between actual employment outcomes of students from Canadian institutions, and their institutions’ Employer Reputation.

Canadian institutions are able to deliver positive graduate outcomes, with graduates securing jobs at high rates, and alumni going on to make a meaningful impact on society. However, Canada’s reputation among employers is significantly lower than these strong graduate outcomes would suggest. Leveraging the successful narratives of graduates will be critical to reversing the decline in Canada’s Employer Reputation.

Rebuilding Employer Reputation will be critical as Canadian institutions fight for market share. In a world where students prioritize graduate outcomes, data-driven narratives that showcase return on investment will resonate with students looking to study in Canada.