.jpeg)

Global Student Flows | Europe

15 October 2025

International education remains one of the most dynamic and transformative global systems of the modern era - a powerful driver of shared growth for learners, destination markets, home countries, and employers. The QS Global Student Flows report presents an evidence-based framework outlining three possible futures for international education through 2030: Regulated Regionalism, Hybrid Multiversity, and Talent Race Rebound. Each scenario explores the impact of geopolitical shifts, technological innovation, demographic change, and economic evolution, providing decision-makers with the insights and tools needed to navigate and shape the future of the sector.

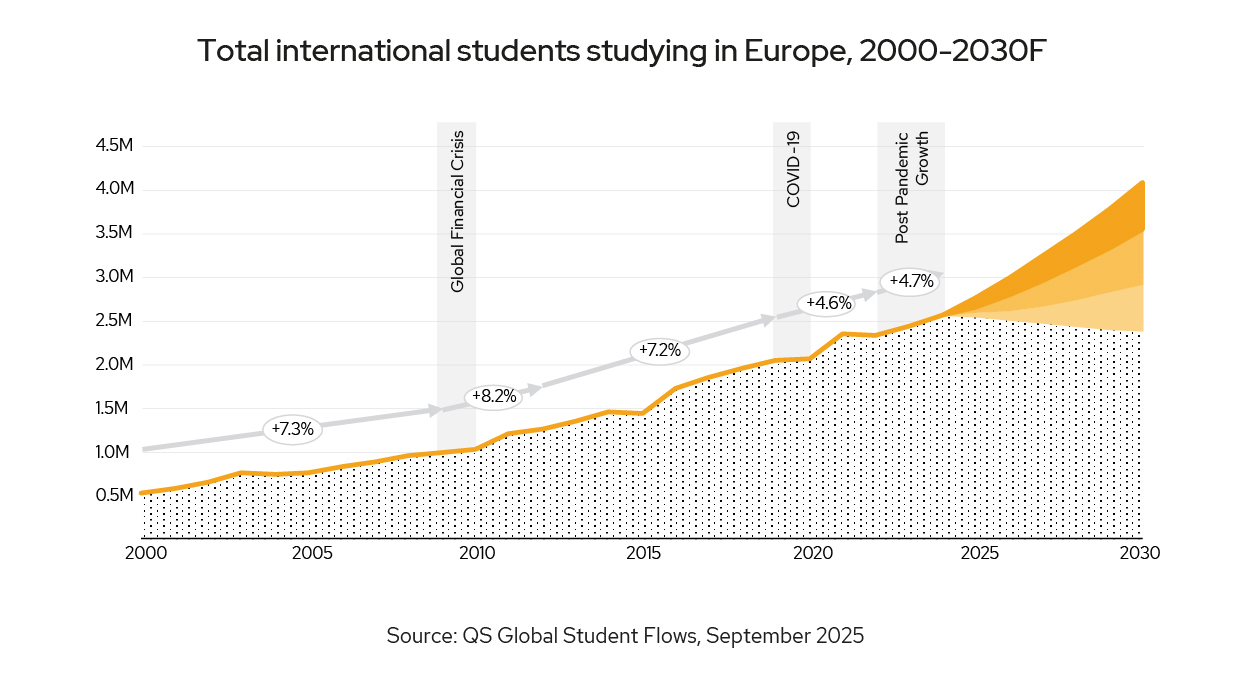

International enrolments in Europe are projected to grow by 5% annually to 2030. While this is a marked slowdown from the 7% annual growth recorded between 2000 and 2024, it remains faster than the US, Canada, Australia and the UK, and Europe’s growth is set to outpace the 4.6% rate it has observed post-COVID. On the whole, European countries are not following the “big four” - the US, the UK, Canada and Australia - in restricting international student visas, thus positioning themselves well for future growth. There are notable exceptions to this – the Netherlands, for one.

Europe stands to benefit from the growing expansion of the African and Asian middle class, and offers affordable study opportunities which these markets continue to value. France, Germany, Italy and Spain’s pivot to offering English-taught programmes has further broadened their appeal as study destinations. Now, continental European countries offer a high-quality education, often taught in English, at a fraction of the cost of the “big four”. According to the QS International Student Survey, 55% of students prioritise affordability when choosing where to study, which reiterates the potential for Europe to benefit from shifting patterns of global student flows. The four largest European destinations – Germany, France, Spain and Italy – will continue to hold the top spots, with all four showing resilient or accelerating post-COVID enrolment growth. Germany leads the continent, buoyed by demand from India, expanding English-taught programmes, and favourable immigration policies, though housing shortages and stretched university capacity pose potential challenges. France benefits from low fees, welcoming government rhetoric, and strong connections with North and West Africa shaped by colonial history, but bureaucracy and debates around migration could hamper demand. International enrolments in Spain and Italy have surged recently, with Spain’s growth fuelled by Latin American demand and Erasmus+ mobility, and Italy’s business and STEM programmes attracting students from Eastern Europe, North Africa, and Asia.

Beyond these four, the Netherlands is tightening capacity, while Austria and Switzerland remain stable. Eastern Europe is increasingly appealing to Asian, Middle Eastern, and African students, especially in medical and health sciences, though its potential depends on investment and reputation.

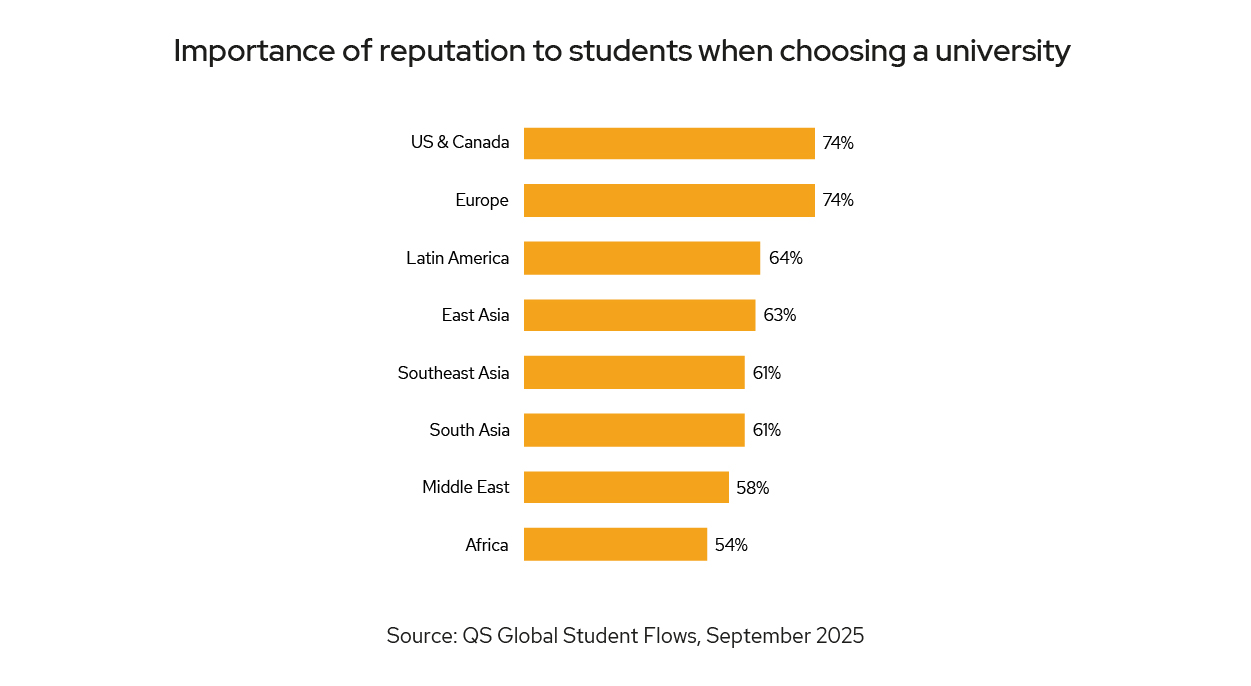

QS International Student Survey data shows that students who want to study in Europe are increasingly looking at the reputation of an institution, and are making decisions based on their prospective career outcomes. This comes as the Academic and Employer Reputation for France, Germany, Italy, Spain is either declining, or plateauing. For key source markets, such as Latin America and East Asia, over 60% of students use reputation as a tool when making study decisions. Reputation is not declining evenly across Europe, with some nations managing to improve their Academic and Employer Reputation; should this continue, these countries may start to take market share from the major European markets.

International students have a crucial role to play as Europe faces labour shortages in in-demand fields. A recent European Commission survey found 63% of small and medium-sized businesses cannot find the talent they require. In the short term, international students can address labour market imbalances during their studies, if countries facilitate this. The QS World Future Skills Index indicates that institutions in several European countries struggle to equip graduates with the skills employers need. To maintain inbound flows, and remain competitive, European institutions must align curricula to industry needs to ensure international graduates join the workforce fully prepared.

This year, we use three evidence-based scenarios as a lens to understand the medium-term outlook for higher education in Europe. Regulated Regionalism: This scenario reflects a future where student mobility is not unrestricted but intentionally guided. Europe remains a major destination, but enrolments are increasingly selective, transparent, and aligned with broader national capacity and regional development goals. The Hybrid Multiversity scenario outlines a model where international students start their education online or in their home countries before travelling to Europe for shorter, focused in-person experiences. These onshore experiences are often linked to hands-on training, internships, or specialised language programmes. Talent Race Rebound sees European countries position international education as a direct pipeline for skilled migration, enabling the continent to proactively address its demographic challenges and ensure it remains competitive in the global race for talent.

Europe’s role in global student mobility is expanding, reflecting both structural demand and shifting policy environments. International enrolments in the region are projected to grow by about 5% a year to 2030 - slower than the 7% annual pace recorded between 2000 and 2024, but still faster than in the US, Canada, Australia, or the UK. In those markets, tighter visa rules and rising costs are constraining demand. Growth to 2030 is set to outpace the 4.6% rate observed post-COVID. Unlike several other major study destinations, international student numbers held steady in many leading European destinations during the COVID pandemic, so Europe is positioned to capture a gradually larger share of global student flows in the years ahead.

Several forces underpin this trajectory. Demographic shifts and the expansion of middle-class populations in Africa and Asia provide a steady pipeline of students seeking affordable, reputable degrees. At the same time, Europe’s ageing population is creating incentives for governments and universities to adopt more open policies, positioning international students as both an economic and strategic necessity. Europe’s relative affordability compared with the big four Anglophone destinations remains an advantage, with public universities in Germany, France, and parts of Southern Europe charging only a fraction of the tuition costs in the US or UK. The proliferation of English-taught programmes has also broadened Europe’s appeal, lowering a barrier that once confined foreign enrolments largely to Francophone, Hispanophone, or German-speaking countries. Erasmus+, with its deep network of institutional partnerships, continues to enable mobility across the continent and into Europe from abroad.

Germany remains the leading study destination within Europe. Over the last two decades, international enrolments in the country expanded at an annualised rate of over 4%, with the post-pandemic years improving on this growth. Between 2025 and 2030, growth is projected to average about 4.5% a year. Demand is led by India - now Germany’s largest source market, ahead of China - followed by Türkiye, Austria, Iran, and a widening pool of students from the Middle East and Africa. Germany’s 2024 Skilled Immigration Act, coupled with rising numbers of English-taught programmes, will strengthen the study-to-work pipeline, reinforcing the country’s appeal for students who see higher education as a path to long-term migration. The main risks remain housing shortages in cities such as Berlin and Munich and the capacity limits of universities already stretched by past expansion. A YouGov poll in February 2025 found that 81% of Germans felt that immigration had been too high over the past decade and support for anti-immigration political parties, such as the Alternative für Deutschland, have increased in recent polls. DAAD has highlighted that only a third of international students feel well prepared to start a career in Germany, with insufficient language skills a key concern.

France offers a similar story of resilience; international enrolments expanded by over 6% annually in the decade before the pandemic, before stabilising at about 3.5% in the years that followed. Looking ahead to 2030, growth is expected to remain broadly in line with this post-COVID trend. France’s appeal lies in its combination of relatively low fees, a government that has explicitly prioritised internationalisation, and strong historical ties and shared language with the Northern and Western African diaspora. Students from Morocco, Algeria, Senegal, and increasingly from Sub-Saharan Africa choose to study in France. The expansion of English-medium programmes has broadened access beyond Francophone markets, though the country’s bureaucratic hurdles and frequent policy debates around migration remain sources of uncertainty.

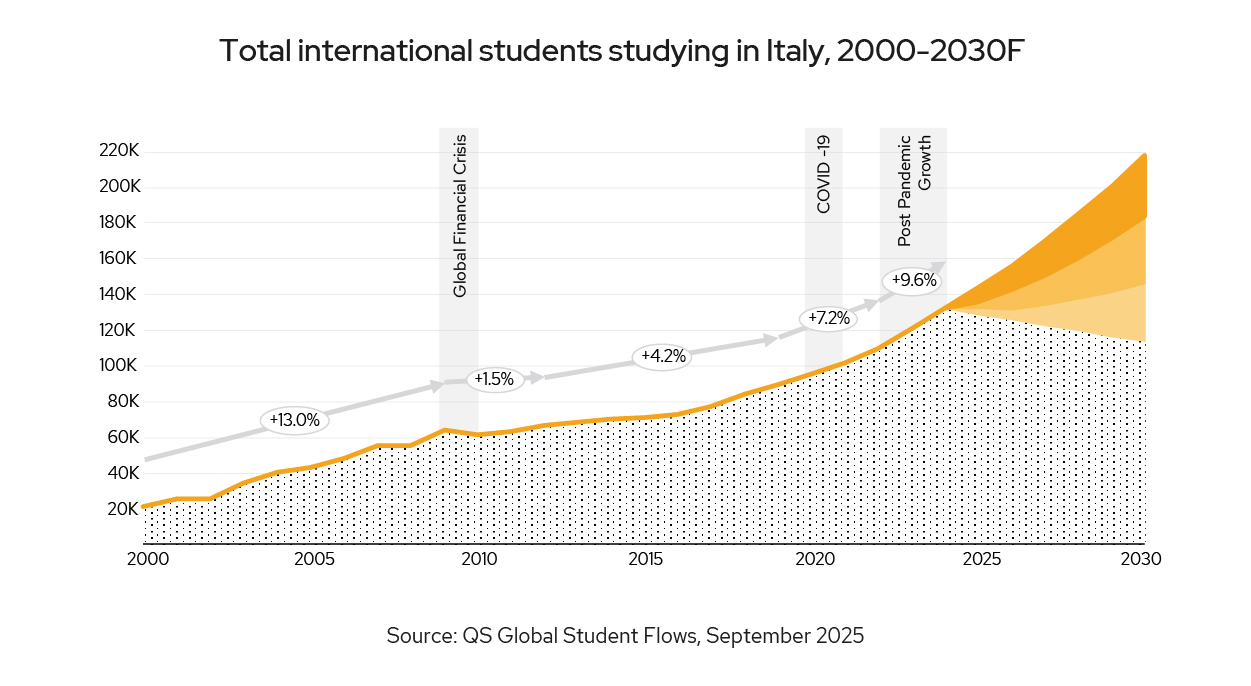

In recent years Spain and Italy have seen some of the strongest growth in foreign enrolments within Europe. In Spain, international enrolments grew by an average of just over 7% per year between 2019 and 2024, with growth accelerating to double digits in the last three years as the sector rebounded from the pandemic. Growth to 2030 is likely to be driven by Latin America and Erasmus+ mobility, though visa changes and housing shortages pose risks. Italy, meanwhile, has expanded by nearly 10% a year since 2022 on the back of English-taught programmes in business and STEM. Demand from Eastern Europe, the Balkans, and North Africa, alongside rising Chinese and Indian numbers, underscores Italy’s growing appeal despite bureaucratic and infrastructure constraints.

Outside the four largest destinations, Europe presents a more varied outlook. The Netherlands, long regarded as a popular destination for foreign students, is tightening controls as universities push back against capacity strains and housing bottlenecks. Switzerland and Austria, by contrast, continue to benefit from reputations for quality and relatively low costs, with steady inflows expected from Germany, Italy, and beyond. However, like in other European countries such as the Netherlands, there have been calls from the Universities Austria (Uniko) to raise the language level requirements for German-taught degree programmes. Eastern Europe presents a more nuanced story; countries such as Poland, Hungary, and Czechia are attracting more medical students from Asia and the Middle East, while Romania and Bulgaria are seeing growth in health sciences programmes. As demand from Africa and Asia continues to expand, the opportunity for Eastern Europe is significant, provided governments invest in capacity and international branding. Risks to the outlook are not trivial. Housing shortages remain the most pressing structural constraint in big cities across Europe, with shortages in student accommodation acute in Germany, the Netherlands, and Spain. Immigration politics represent another wild card. While Europe as a whole is more open than most Anglophone destinations, rising populist pressures could trigger sudden restrictions. Competition is also intensifying. Asia, particularly China and Malaysia, is expanding its own international education capacity, while digital provision - especially English-language online programmes - provides alternatives to physical mobility. To add to this, demographic change within Europe means that domestic enrolments are stagnating or shrinking, leaving institutions ever more dependent on foreign inflows. Even so, Europe’s fundamentals remain strong. With projected growth of around 5% a year to 2030 - higher than any of the traditional Anglophone destinations - the continent looks set to deepen its role as a global education hub.

.jpg)

The Global Student Flows (GSF) initiative comprises three core components: QS’ Open Source Framework for Global Student Flows, a proprietary Flow Mapping and Analytics Technology, and a Scenario-Based Forecasting Methodology designed to simulate over 4,000 discrete source-to-destination flows. Together, these instruments offer a comprehensive, 360-degree view of the global outlook for international student mobility.

The QS International Student Survey offers an unparalleled view into pre-enrolled international students. The 2025 iteration draws on responses from over 70,000 students in 191 locations. The questions in the Survey are designed to enable higher education institutions to make sound decisions on recruitment and communication strategies. Now combined with Global Student Flows data, we offer a well-rounded view of where students are choosing to study, and how they make that decision.

Access more information about the methodology in the full report.

Germany, France, Italy and Spain in focus

Germany has long been one of Europe’s engines of international student mobility, and its numbers reflect a two-decade surge. From 2000 to 2024, the number of international students grew at an average annual rate of over 5.5%, as Berlin’s low-cost universities and reputation for quality engineering and applied sciences drew students from across the globe. Even the pandemic did not derail momentum; between 2019 and 2024, numbers still expanded by 4.8% a year.

Looking ahead, growth is projected at around 5% annually through to 2030, leaving Germany with an expanding student body supported by strong underlying fundamentals. The new Skilled Immigration Act, which eases pathways from study into work, is a powerful draw for students who see Germany not just as a degree destination but as a gateway to Europe’s labour market. Tuition remains minimal, particularly at public universities, a critical advantage against competitors such as the US, UK, and Australia – indeed 63% of those looking to study in Germany prioritise affordability, a figure which is significantly higher than those looking to study in the UK or Australia (QS International Student Survey 2025). The proliferation of English-taught programmes at the master’s level - now numbering in the thousands - widens Germany’s reach well beyond traditional German-speaking markets.

While the overall pool of source markets is broad, several countries will likely continue to dominate in volume. India has emerged as the largest single origin, overtaking China in recent years, and will continue to expand on its demographic strength and Germany’s appetite for STEM talent. North African countries - Egypt, Morocco, and Tunisia in particular - are also sending increasing cohorts, encouraged by geographic proximity and shared history.

Risks to this outlook are equally clear. Housing shortages have become a structural bottleneck in university cities such as Munich, Berlin, and Frankfurt, where rents are surging faster than student stipends. Some 60% of students looking to study in Germany now worry about finding suitable accommodation, making it the second largest concern for students, after the cost of living (QS International Student Survey 2025). Research from the 2024 MLP Studentwohnreport found that on average costs of typical student rents rose by 5.1% between 2023 and 2024. While average rental costs in Berlin and Leipzig rose by 9.4% and 9.3%, other popular student cities such as Würzburg and Tübingen only increased by 1.6%. Immigration bureaucracy remains cumbersome, with visa appointments and residence permits subject to long delays. Competition within Europe is heating up; Italy and Spain are expanding English-language provision aggressively, while France retains its dominance among francophone students.

The net result is a period of steadier, sustainable growth rather than another surge. Germany is likely to remain a top-tier destination - reliable, affordable, and employment-oriented, with the reputation of its institutions among employers consistently and significantly exceeding that of institutions in France, Italy and Spain, according to the QS World University Rankings.

The outlook for student mobility to France is positive to 2030, with growth likely to average around at 4-4.5% a year through the second half of the decade.

In the decade before COVID, foreign enrolments grew at over 6% annually but comparatively slowed in the second half of that decade. During the pandemic and its aftermath, growth held at 3.5% a year on average. In the upcoming period, France will likely consolidate its role as Europe’s second-largest destination after Germany.

Three drivers stand out: First, affordability; even with the introduction of higher fees for non-EU students in 2019, France remains one of the most cost-effective major destinations, significantly cheaper than the key Anglophone destinations, with tuition and living costs well below the UK. This is reflected in student concerns, with 71% of students interested in studying in France citing cost of living as their principal source of anxiety. Second, policy support; the “Bienvenue en France” initiative has pumped resources into scholarships, visas, and marketing in priority regions. Third, demographics; Africa’s fast-growing youth population, especially in Francophone countries, provides a structural source of demand unmatched by any other European country.

The composition of France’s international student body underscores these trends. In the QS Global MBA Rankings 2026, six French business schools rank in the global top 15 for diversity, the indicator measuring the international make up of student intakes and faculty. Morocco, Algeria, and Tunisia remain the top sources in North Africa, all ranking among the top five source markets for France overall. Beyond Africa, China and India are important, with China being the third largest source market for France. The government is signalling a clear interest in strengthening its relationship with India as a counterbalance to its traditional reliance on Francophone countries; a target of 30,000 Indian students in France by 2030 was announced in January 2024. This push is expected to boost India’s rank from 13th to 10th among foreign student populations.

Yet there are headwinds. France lags behind Germany, Italy, and Spain in the share of English-taught programmes, a crucial weakness in markets where French is not widely spoken. Communicating and studying in English is more of a concern to students looking to study in France than it is for students in other destinations (QS International Student Survey 2025). Bureaucracy remains a perennial complaint, from residence permits to housing allocation, and recent tweaks to visa rules may create additional friction. Housing shortages are particularly acute in Paris and Lyon, with rising rents increasingly pricing out students from lower-income backgrounds. Overall, France is likely to continue to thrive on affordability, soft power, and Africa’s demographic momentum.

Italy’s international student flows are expected to grow at a moderate but steady pace, averaging over 5.5% annually in the next five years, led by strong demand from regions like Iran, Africa, China, and Türkiye. The outlook reflects a combination of relatively low tuition fees, more affordable living costs than in Northern Europe, and the rapid expansion of English-taught programmes, which have made Italy the fifth-largest provider of such courses in Europe – 60% of those looking to study in Italy prioritise affordability when making study decisions, reiterating its ability to harness the potential from shifting student flows. Demographic pressures, including an ageing population and declining birth rate, are also pushing Italian institutions to become more open to international students than in the past. Still, bureaucratic friction and strict visa requirements continue to make the process less smooth than in competing EU destinations such as Germany or France.

Policy reforms are an important driver of this growth outlook. The 2023 Decreto Cutro marked a turning point by removing quota limits on converting study permits into work permits, a significant change over the previous Decreto Flussi system, which restricted opportunities. This policy change strengthens Italy’s attractiveness, even though the country still lags behind Germany and France on longer-term migration pathways, with graduates in Italy given just 12 months of post-study stay compared to 18 and 24 months, respectively. This is reflected in student priorities, with only 26% of those looking to study in Italy prioritising post-study work opportunities – a figure which is significantly higher for those looking to study in Germany and the UK (QS International Student Survey 2025). The new biometric requirements for visa applicants reflect standardisation with other EU states but add administrative hurdles that may slow inflows from some regions. Overall, reforms suggest Italy is moving toward greater openness, though progress remains more incremental than transformative.

Türkiye and Iran are currently the strongest drivers of inflows, with rising tuition costs and political instability at home pushing students abroad, while Italy’s affordability and scholarships such as “Invest Your Talent in Italy” serve as key pull factors. Diversifying the source of international students would be an important goal for Italy, as an over-reliance on any single country could pose a risk to long-term growth. This is especially true for source countries that face external pressures, like Iran, where political instability or other factors could lead to an increase in asylum seeker or refugee claims. While this is not an immediate problem for Italy’s student pipeline, it highlights a key structural consideration for ensuring sustainable and stable foreign student inflows over time.

African student numbers - especially from Morocco, Tunisia, and Egypt - are on the rise, drawn by shared history and language, cost advantages, and the growing availability of English-taught programmes. Tunisian enrolments, for example, are expected to grow by 5% annually, up from a pre-pandemic 10- year average growth of 2%. The expansion of initiatives like Erasmus+ to include North African nations has further strengthened mobility from the region. Chinese demand remains steady at a growth rate of just over 1%, concentrated in art, fashion, and design fields, supported by targeted pathways such as the Marco Polo and Turandot schemes. Within the EU, Romanian students continue to represent a significant share of inflows, benefiting from freedom of movement and Italy’s well-regarded programmes in medicine and architecture.

Housing remains a critical challenge that could limit growth despite strong demand – nearly 60% of students looking to study in Italy cite concerns about housing availability as one of their principal worries. However, major Italian cities face shortages. Italy’s National Recovery and Resilience Plan targets 60,000 new student beds by mid-2026, yet demand is anticipated to surpass supply even once these additions are completed. On the academic side, however, the expansion of English-taught programmes has been a powerful growth driver, removing one of the country’s traditional barriers for non-Italian speakers. Combined with lower tuition and living costs compared with many Northern European destinations, Italy is emerging as an increasingly attractive and accessible option, particularly at a time when some countries, such as the Netherlands, are scaling back English-taught offerings.

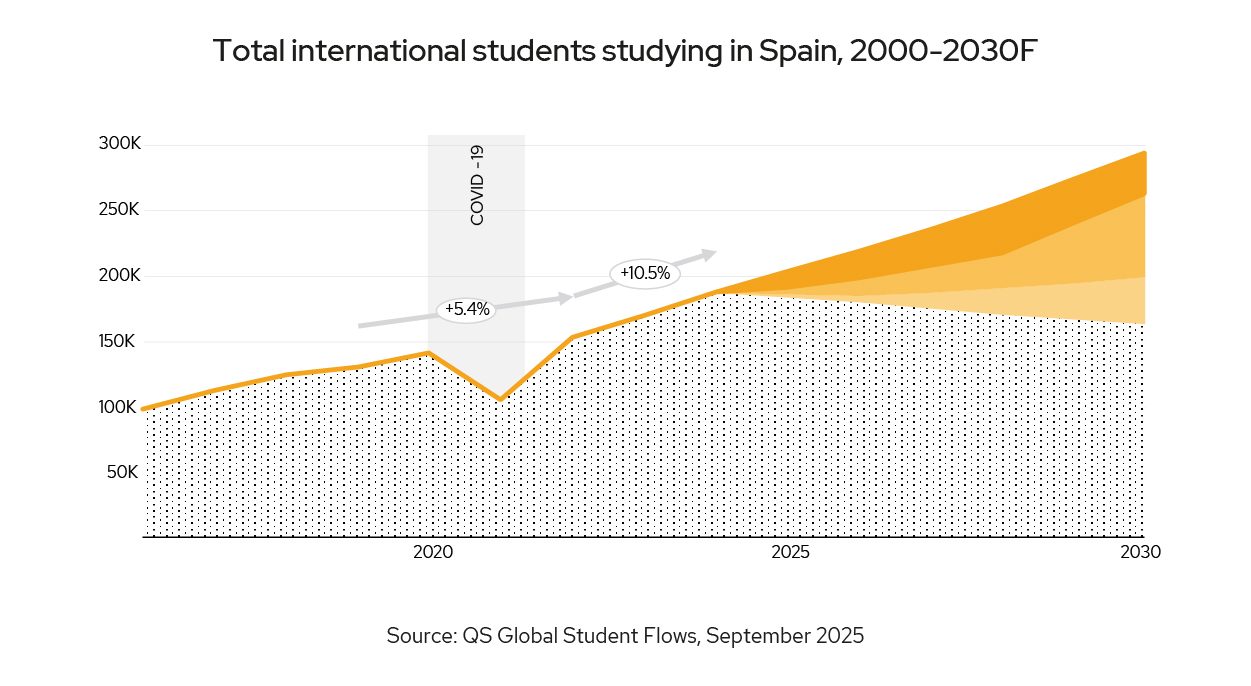

Spain is projected to see international student flows grow by more than 5% over the next five years, with a strong appeal across Latin America, Africa, and Europe, driven by recent policy reforms and expanded post-study opportunities.

The government has made it easier for international students to support themselves and transition into the labour market by increasing permitted work hours from 20 to 30 hours per week and removing the three-year residency requirement to switch from a student visa to a work permit. This is reflected in student priorities, with 48% of those interested in studying in Spain citing concerns about getting a job and 40% prioritising the graduate employment rates of their courses – both significantly higher than for other European destinations. Longer permit validity has reduced bureaucratic hurdles, while new visa provisions open opportunities for international students and specifically target those who have been restricted from the US or cannot complete their studies there due to visa suspensions. Simultaneously, while authorities have implemented restrictions on short-term language courses, including minimum age requirements, a new two-year study cap, and a ban on converting from such permits into work visas signals a clear shift toward attracting degree-seeking students who are more likely to remain and contribute to Spain’s economy.

Latin America is set to remain one of Spain’s fastest-growing source regions at an average growth rate of close to 5%, led by Colombia, Mexico, Ecuador, and Peru, as shared language, cultural ties, affordable tuition, and tightening US visa restrictions redirect demand. Africa is also a significant growth driver, having grown at a rate of 14% annually since 2017. The growth outlook remains strong under Spain’s “Focus Africa 2023” strategy launched in 2021, with Morocco, Algeria, and Nigeria targeted to strengthen both educational and economic links.

Within Europe, Spain’s position as the top Erasmus+ destination secures steady inflows from Italy, France, and Germany, while together these countries, along with the US, Colombia, Mexico, and Ecuador, account for nearly half of Spain’s international student population. Beyond these core markets, Spain is drawing greater interest from South Korea, Japan, and Canada, where students are attracted Global Student Flows: Europe 22 by affordability, easier visa pathways, and the option to study in Europe when access to the US is more restricted.

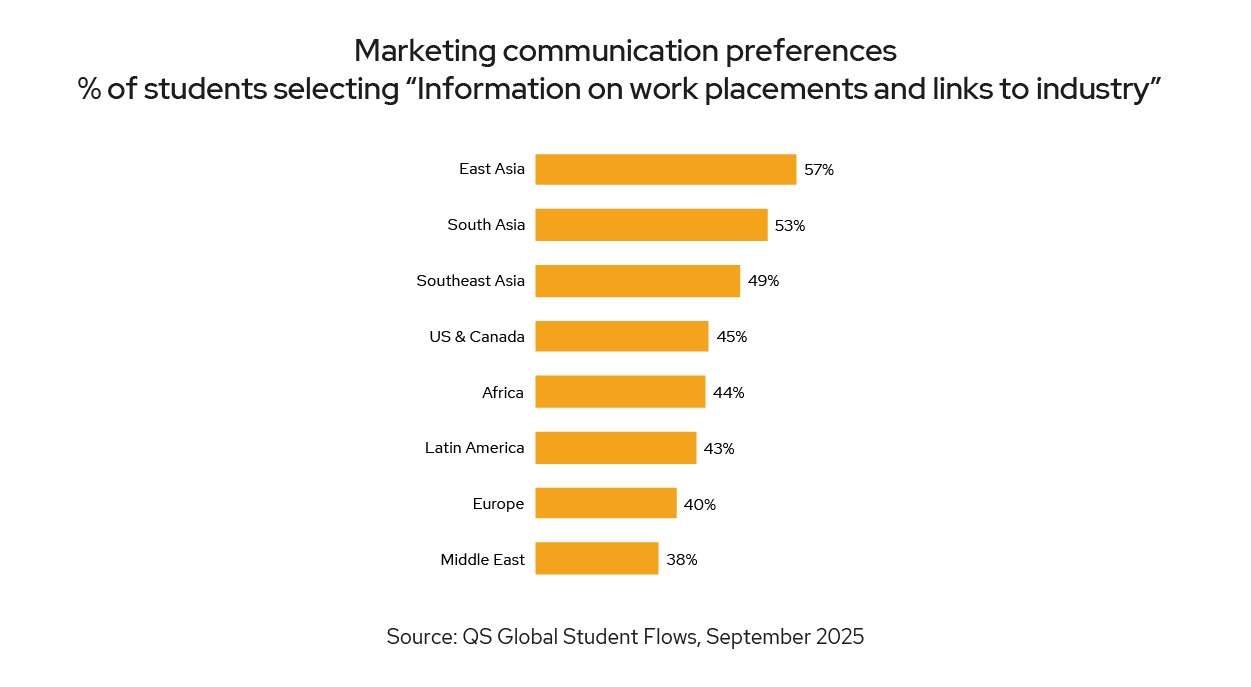

Spain competes most directly with Germany, France, and the Netherlands in the EU. Germany and France remain attractive due to low tuition and global academic prestige, while the Netherlands has pulled back slightly in response to housing shortages and social integration concerns. Spain’s edge lies in combining relatively affordable tuition with stronger work rights and clearer post-study residency opportunities, making it an increasingly competitive choice for degree-seeking students. Some 47% of those looking to study in Spain cite information on work placements and links to industry as one of their preferred marketing communication topics, a figure which is significantly higher than for other European destinations. Its continued leadership within Erasmus+ further cements its role as a major hub for intra-European mobility.

Regulated regionalism in Europe represents a strategic and centrally coordinated approach to student mobility, balancing the regional frameworks with the autonomy of member states. Moving away from an unregulated global market, it prioritises the creation of a cohesive, internal European Higher Education Area (EHEA) while also leveraging international students to address specific regional economic and demographic needs.

Europe’s model of regulated regionalism is a direct result of policies designed to integrate member states’ higher education systems. The Bologna Process and its standardised degree structure (Bachelor, Master, PhD) are foundational, ensuring that academic qualifications are easily recognised across borders, enabling seamless intra-European student mobility. The Erasmus+ programme serves as a financial and administrative mechanism, offering grants and structured pathways for students to study or train in another EU country. These frameworks create a transparent, predictable environment for mobility within the bloc, reducing barriers and encouraging a self-contained flow of talent.

While major academic hubs like Germany and France remain popular, regulated regionalism is also driving growth in emerging destinations. Countries such as Spain, Poland, and Hungary are increasingly attracting students from both within and outside the EU due to their lower tuition fees and cost of living.

Furthermore, Europe is becoming more intentional about attracting and retaining international students to fill specific workforce gaps. New policies, such as the EU Talent Pool and the Blue Card, aim to streamline migration pathways for highly skilled graduates. This signals a strategic shift from simply attracting students for their economic contribution to aligning student mobility with regional labour market needs. Enhanced visa scrutiny and enrolment management ensure that mobility supports genuine academic goals and contributes to long-term workforce planning, rather than being solely market-driven.

This scenario reflects a future where student mobility is not unrestricted, but intentionally guided. Europe remains a major destination, but enrolments are increasingly selective, transparent, and aligned with broader national capacity and regional development goals.

This scenario outlines a model where international students engage in a blended learning approach, starting their education online or in their home countries before travelling to a European country for a shorter, focused in-person experiences. These onshore experiences are often linked to hands-on training, internships, or specialised language programmes.

Under this model, students begin their academic journey remotely, leveraging online platforms or local partner universities within their home countries. Courses are designed to meet the academic standards of the host European university, with robust credit transfer systems ensuring a seamless transition between the offshore and onshore phases of study. Universities formally recognise micro-credentials earned during the initial stages, allowing students to build their qualifications progressively. The final stages of study in Europe could include capstone projects or industry-linked experiences to facilitate a smooth transition into the workforce.

The Erasmus+ programme would evolve beyond its traditional focus on physical student exchange to support a more flexible and integrated system of transnational education. To support this new model, European universities would actively adapt their campuses and digital infrastructure. Physical campuses would be reserved for activities that require hands-on learning, such as laboratory work, design studios, or direct employer engagement. At the same time, digital infrastructure would be significantly strengthened to provide a high-quality, immersive learning experience for students beyond Europe.

The Hybrid Multiversity scenario is particularly attractive for European countries as it can help manage migration and infrastructure pressures while maintaining global academic engagement. By offering qualifications through universities and partnerships in countries across Africa, Asia, and Latin America, Europe can build a pipeline of skilled individuals while generating revenue and fostering long-term academic and cultural ties. This model offers a more affordable and flexible alternative to traditional full-onshore degrees, making European education more accessible to a wider pool of international talent. However, widespread adoption would require collaborative efforts among EU member states to align visa and education frameworks to support this innovative approach.

Europe would increasingly view international education as a strategic tool for addressing its significant skills shortages and demographic challenges. Consequently, Europe is redefining international education as a targeted pathway to attract and retain highly skilled talent in priority sectors, positioning students as future contributors to the EU workforce and economy.

Under this model, European countries would adjust their policy settings to adopt a more targeted approach. While general student intake might be managed more closely, exemptions and streamlined processes would be provided for priority groups, such as those in high-demand fields like fields like IT, healthcare, and engineering.

The EU’s Blue Card Directive, which offers a residence and work permit for highly-qualified non-EU citizens, would be a key mechanism in this strategy. The policy could be further streamlined to be more flexible, with criteria aligning more closely with specific national workforce needs. For example, countries with acute shortages of engineers could offer a lower salary threshold or faster application processing for engineering graduates.

To better align student pathways with labour market needs, post-study work rights would be redesigned to favour graduates entering sectors with critical shortages. The EU’s Talent Pool initiative, an online platform to match non-EU job seekers with employers, would be integrated with the education system. International graduates with European qualifications and local work experience in a high-demand field would earn additional points in a potential EU-wide or national-level migration points system. This creates a clear and appealing pathway for students from countries where international study is seen as a route to long-term stability and economic opportunity.

By positioning international education as a direct pipeline for skilled migration, Europe can proactively address its demographic challenges and ensure it remains competitive in the global race for talent.

Using insights into what students want to future-proof your strategy

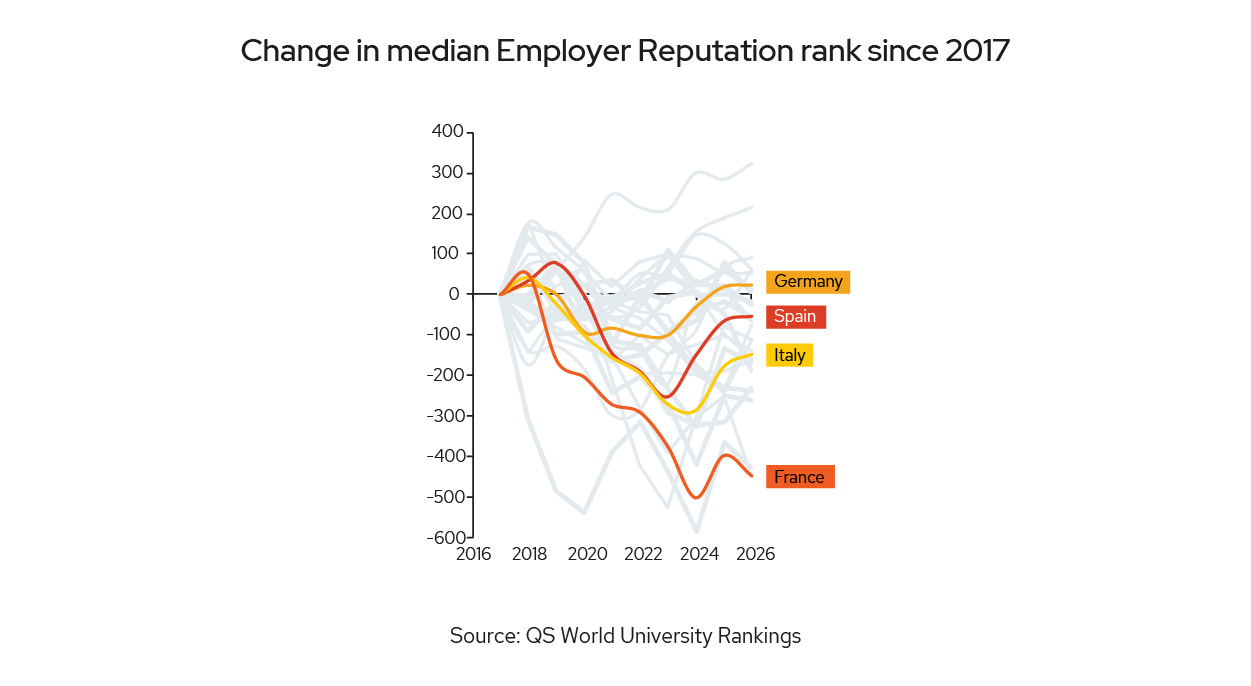

While the Global Student Flows forecast for the major continental European destinations is relatively positive, there are possible concerns on the horizon. Students are increasingly looking towards reputation and career outcomes when making study decisions; at the same time, the Academic and Employer Reputation rank of these countries is plateauing, or, in some cases, rapidly declining. The median Employer Reputation rank of French institutions has dropped by nearly 500 positions between 2016 and 2026.

The majority of all students, regardless of source market, see reputation as important when choosing a European university . For the markets that send the most students to Europe, such as Latin America, East Asia and Southeast Asia, over 60% of students use reputation as a guide. This heightens the risk facing institutions in France, Germany, Italy and Spain as they battle with declining and plateauing reputation. This is particularly alarming when these charts show that this reputational decline has not been seen across Europe, with many nations managing to improve their average Academic and Employer Reputation.

.jpg)

With heightened competition from other European countries, and students increasingly looking for reputable institutions that improve their employment prospects, France, Germany, Italy and Spain will need to build their reputation and outperform their European peers to mitigate risk.

Students are increasingly focusing on post-study employment outcomes when considering international study. Regardless of source region, the majority of students looking to study in Europe say that the ability to learn new skills is an important career consideration for candidates. Prospective students see their time at university as an ideal time to upskill and articulate the value they can add to employers.

Information about work placements and links to industry was identified as useful when making study decisions by 43% of students. This information was deemed more useful by students from East, South and Southeast Asia. with 640,000 students forecast to study in Europe from these regions, it is key European institutions get this messaging right, and focus on the metrics that matter to students.