.jpeg)

QS Global Student Flows

1 July 2025

International education remains one of the most dynamic, high-impact global systems of the modern era; a powerful force that delivers shared prosperity for learners, destination markets, home countries, and employers alike. The QS Global Student Flows report offers an evidence-based framework outlining three scenarios for international education through 2030—Regulated Regionalism, Hybrid Multiversity, and Talent Race Rebound. Each scenario considers geopolitical developments, technological advancements, demographic shifts, and economic transformations, equipping decision-makers with the tools needed to anticipate and adapt to the future.

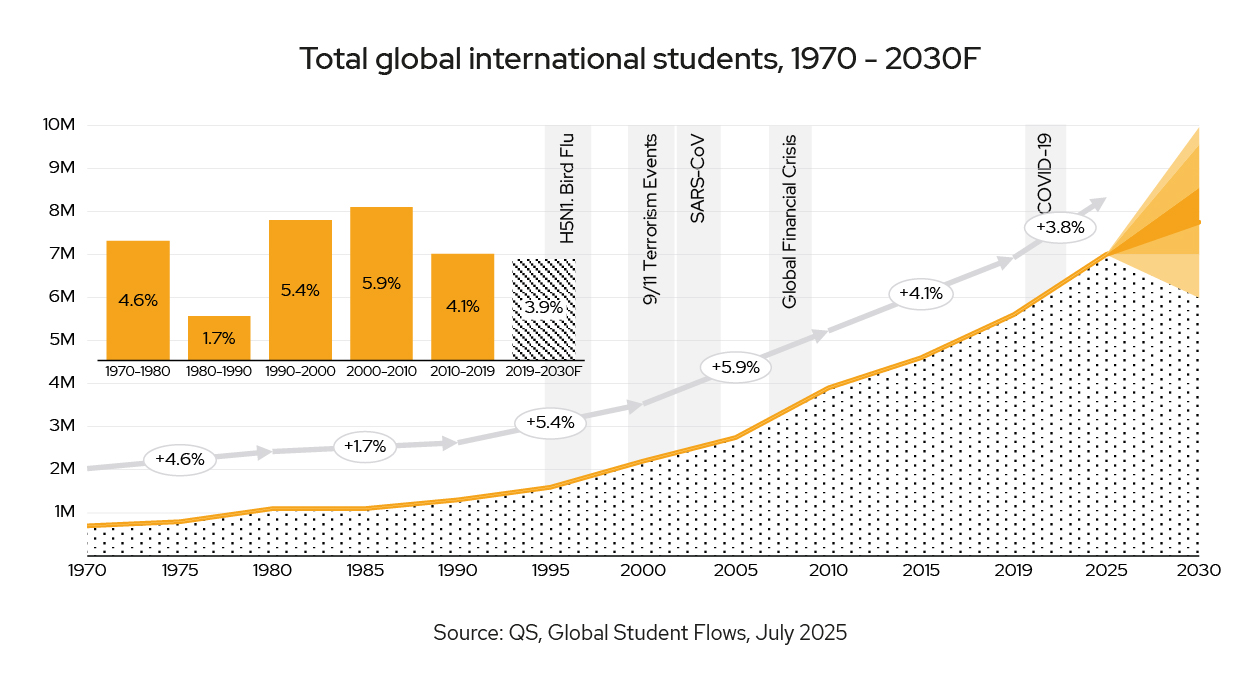

Global student demand for international education remains robust, continuing its historical trajectory with an estimated annual growth rate of approximately 4% over this decade. By 2030, the total international student population is projected to reach approximately 8.5 million. Despite this consistent upward trend, the global student mobility landscape is marked by considerable uncertainty driven by shifting geopolitical climates, evolving economic conditions, and changing student preferences. Consequently, traditional market leaders now face heightened competition from emerging education destinations.

Between 2020 and 2025, student priorities significantly evolved, reflecting a deeper focus on outcomes and institutional reputation. Attending a leading university has become increasingly critical, with academic and employer reputation seeing increased emphasis. Students also prioritise opportunities to establish robust personal and professional networks, recognising the long-term value of strong connections. Additionally, the attractiveness of a country’s culture and lifestyle has grown in importance, indicating a rising significance placed on comprehensive student experiences beyond academics alone. The general reputation of a destination as welcoming, alongside demonstrably high-quality teaching standards measured through rankings and benchmarks, further shapes student decision-making.

To navigate the uncertainty influencing global student flows, this report outlines three distinct scenarios. The first scenario, Regulated Regionalism, anticipates stricter national frameworks resulting in more concentrated regional student mobility. In this model, traditional anglophone destinations such as the US, UK, Canada, and Australia might encounter tighter enrolment restrictions, while emerging hubs, particularly in Asia and the Middle East, could significantly expand their market share.

The second scenario, Hybrid Multiversity, emphasises digitally-enabled, hybrid educational models combining local, remote, and brief international study phases. Driven by economic uncertainties and technological advancements, this scenario reflects a growing preference among students for flexible and cost-effective education pathways. Institutions capable of rapidly adapting their offerings to include robust digital and hybrid learning options are likely to thrive in this scenario.

The third scenario, Talent Race Rebound, portrays intense global competition for international students, driven by demographic pressures and acute labour shortages. Countries adopting streamlined visa processes, enhanced post-study work rights, and significant investments to attract global talent—particularly in science, technology, engineering, and mathematics (STEM) fields—are poised for substantial growth. Under this scenario, leading traditional markets such as the US, UK, Australia, and Canada could regain strong growth trajectories through proactive immigration policies and deeper industry collaboration.

Each scenario presents distinct strategic implications for institutions in major markets. In a Regulated Regionalism environment, traditional destinations might experience restricted growth due to policy and capacity constraints, prompting student flows toward new regional education centres. Under Hybrid Multiversity conditions, institutions in established markets would need to quickly shift to a flexible learning model and forge partnerships with the rapidly improving institutions in students’ home markets. If the Talent Race Rebound scenario comes to pass, institutions in major markets will have to work hand in glove with governments and industry to attract talent in a competitive environment.

In this time of rapid global change, the Global Student Flows initiative, established in 2018, continues to accelerate its mission to map, forecast, and guide international education strategy for governments, institutions, and the broader global talent ecosystem. This year’s report introduces three future scenarios for international education through to 2030, shaped by thousands of conversations with leaders across government, education, and industry, and grounded in insight from more than 70,000 students from 191 locations looking to study at 146 institutions. Together these scenarios offer a robust, evidence-based framework to navigate a sector at the intersection of geopolitics, demography, technology, and labour market transformation.

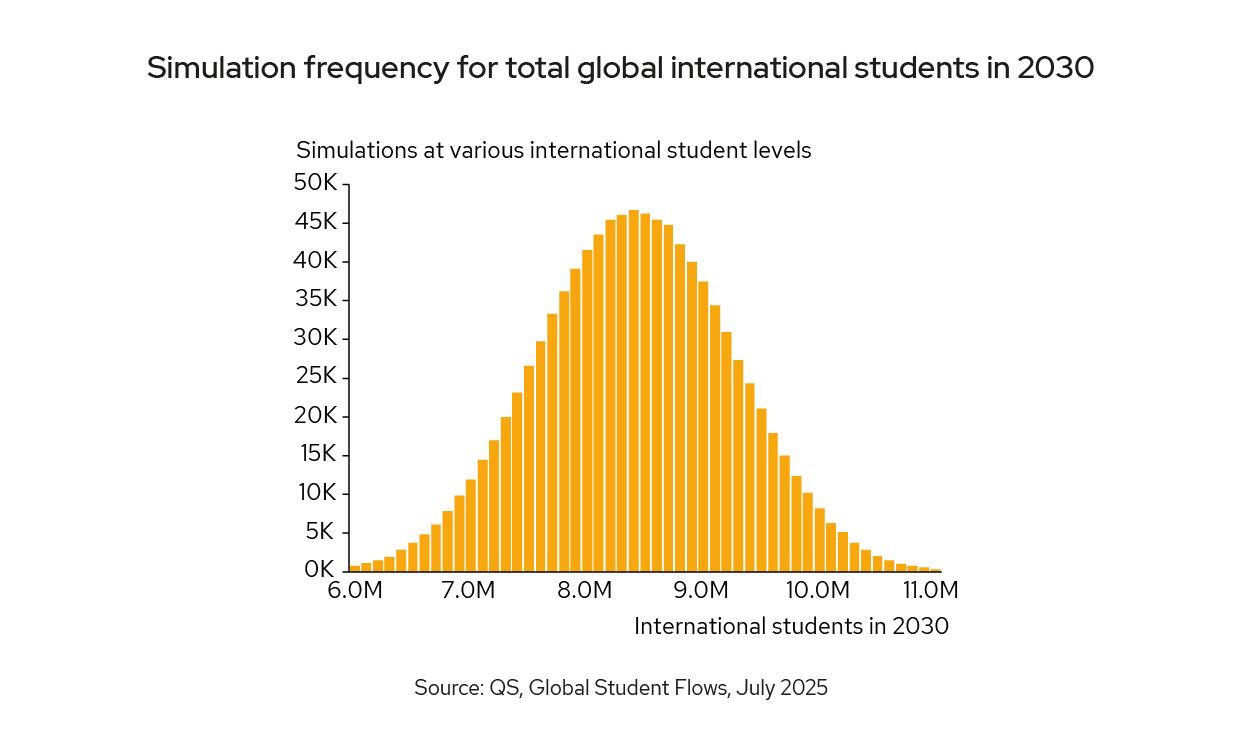

Our 2025 forecast projects approximately 8.5 million international students by 2030, representing a compound annual growth rate just below 4%, the long-term historical trajectory over the past five decades. Drawing on hundreds of expert interviews and advanced simulation analysis, we estimate a 95% confidence interval ranging from six to 10 million international students in 2030. This range reflects both plausible headwinds, such as political disruption or economic fragmentation, and tailwinds like a global race for talent or the rise of new, attractive study destinations.

As we look ahead, it is also important to reflect back. In 1970, fewer than one million students crossed borders to pursue education. Today, more than seven million students are part of a globally connected academic ecosystem, exchanging knowledge, building relationships, and contributing to economies around the world. This dramatic expansion of international student mobility is not just a story of scale, but of strategic significance.

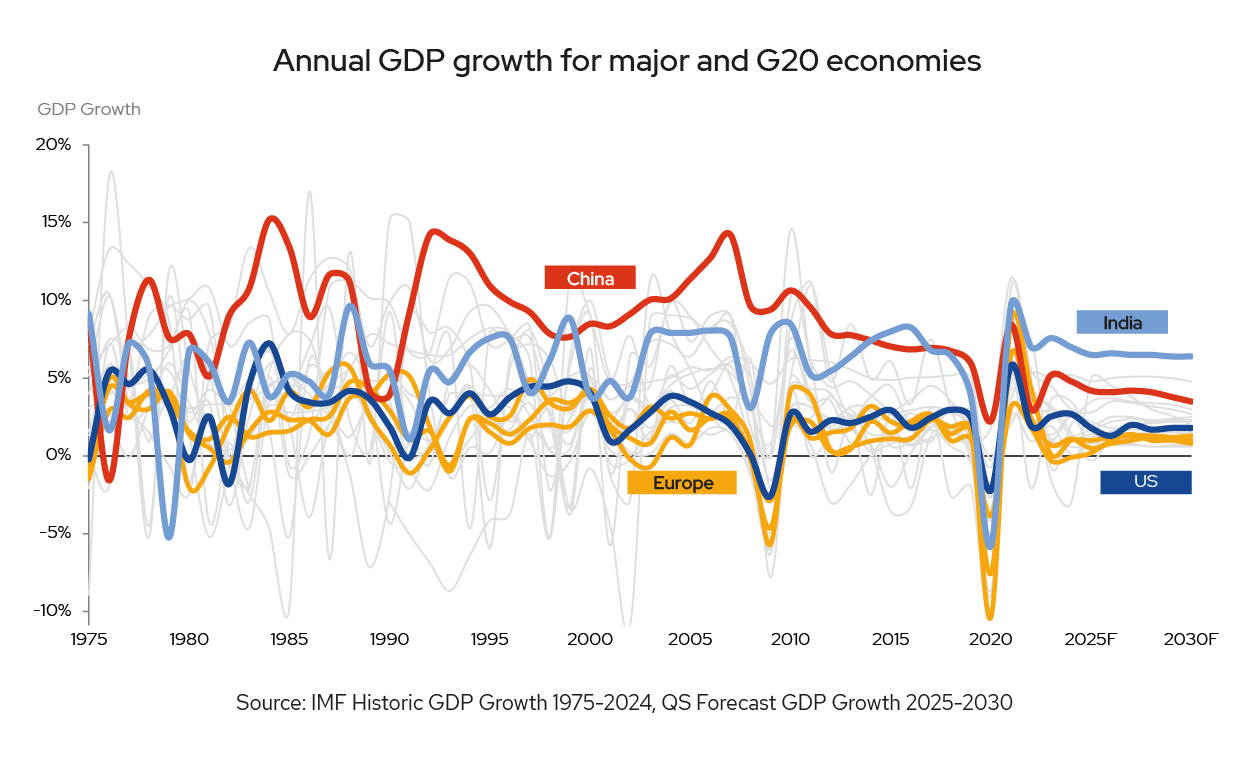

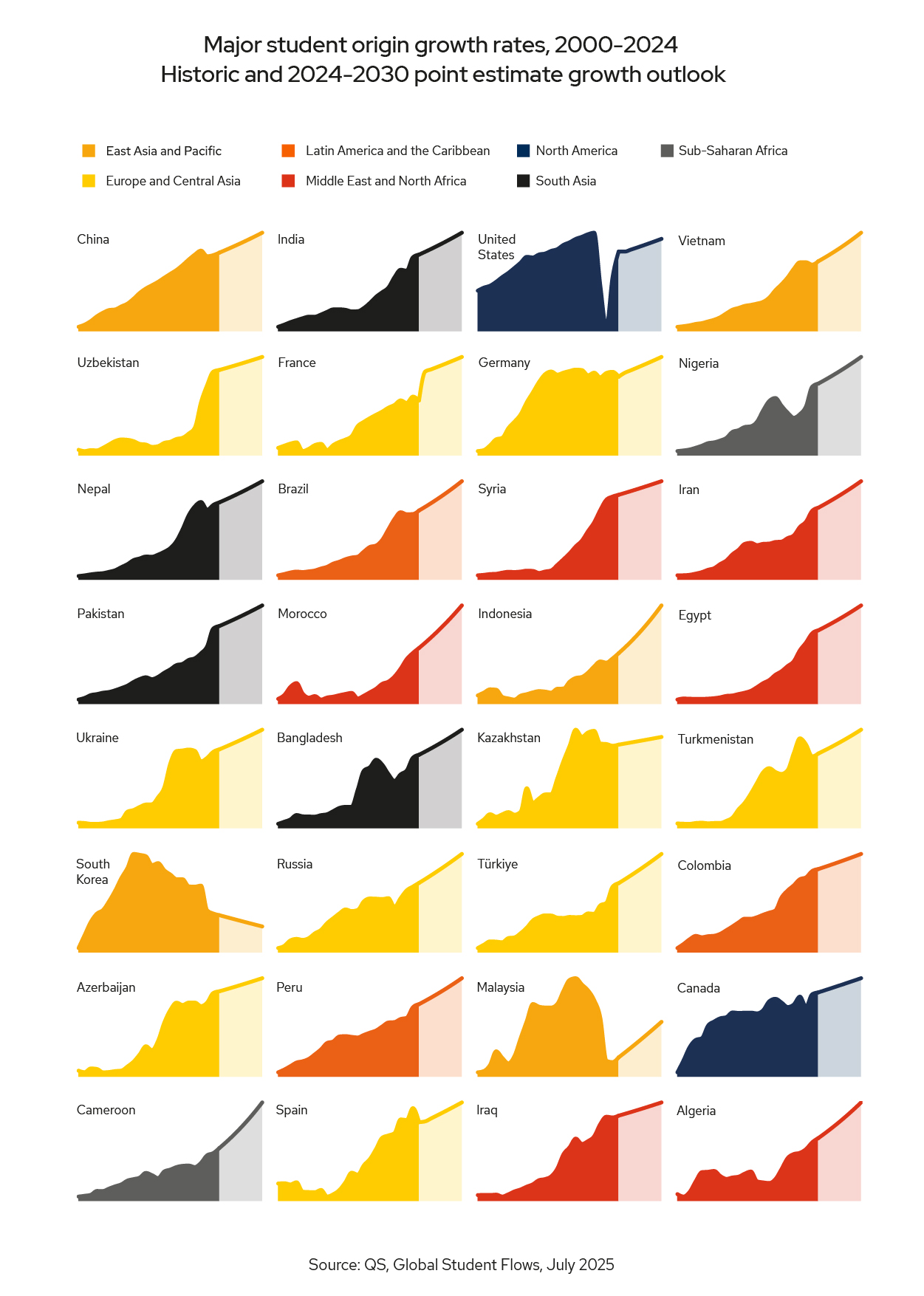

The evolution of global student flows reflects the evolution of the global economy. Over the past five decades, China has emerged as one of the most influential stakeholders in global education, both as a leading sender and, increasingly, as a study destination. India, with its demographic dividend and expanding middle class, continues to accelerate as a driver of outbound mobility, and is projected to shape the global student population for decades to come as more institutions from around the world seek to become part of India’s domestic higher education landscape. At the same time, traditional destinations such as the United States, the United Kingdom, Canada, and Australia have experienced both growth and turbulence. Much of this stems from domestic policy shifts, immigration frameworks, and international competition. Meanwhile, emerging destinations, principally across Asia and the Middle East, are stepping onto the global stage, offering new pathways and models for student success.

The one constant across these transformations is the central role of talent. Nations and institutions that recognise the strategic importance of attracting, nurturing, and retaining global talent will be better positioned to thrive amid increasingly complex dynamics. International education stands at the heart of this equation, bridging cultures, building capacity, and empowering the next generation of leaders, researchers, and innovators.

The Global Student Flows Initiative, now in its eighth annual cycle, serves as a strategic guide for those navigating this complexity, providing not just forecasts but deep foresight into the forces shaping global education, mobility, and talent for the years to come.

The Global Student Flows (GSF) initiative comprises three core components: QS’ Open Source Framework for Global Student Flows, a proprietary Flow Mapping and Analytics Technology, and a Scenario-Based Forecasting Methodology designed to simulate over 4,000 discrete source-to-destination flows. Together, these instruments offer a comprehensive, 360-degree view of the global outlook for international student mobility.

The QS International Student Survey offers an unparalleled view into pre-enrolled international students. The 2025 iteration draws on responses from over 70,000 students in 191 locations. The questions in the Survey are designed to enable higher education institutions to make sound decisions on recruitment and communication strategies. Now combined with Global Student Flows data, we offer a well-rounded view of where students are choosing to study, and how they make that decision.

Access more information about the methodology in the full report.

Teaching quality, university reputation and lifestyle are key priorities when students are deciding on a study destination.

The top priorities for students when choosing a country, according to the QS International Student Survey 2025

The last five years have seen institutional reputation (and therefore university ranking performance), graduate outcomes and post-graduate employment all become increasingly important to prospective students. The desire for strong post-graduate outcomes is further emphasised by their worries about studying abroad. 67% of students said cost of living was a concern; getting a job was identified as a concern by nearly 50% of respondents. Crucially, respondents want universities to help: 62% of respondents said that a university having a money advice service was very or extremely important.

Developed economies across Europe and maturing key source markets of India, Nigeria, Türkiye and Brazil have seen cost of living dropping in importance. However, if global economic growth slows as predicted, this trend may slow or reverse entirely.

A student’s personal interest and the passion they have for their chosen subject remains a critical component that guides their decision-making. However it’s clear that learning for the sake of learning is no longer the sole driver amongst this audience. A combination of economic realities and cost of living pressures means that prospective students are increasingly prioritising their future career planning when deciding what and where to study. Whilst students would still expect that personal interest in the subject to be reciprocated by their teachers and lecturers, they would also expect their learning experience to be oriented around their future skills development and career pathways.

Globally, a personal interest in the subject used to be the most important factor when choosing a course. However its importance has declined from 61% in 2020 to 50% in 2025.

A personal interest in the subject remains important, but has made way for other priorities such as the graduate employment rate and institutional reputation. The shrinking focus on personal interest in the subject is most evident in a number of African markets, where it is increasingly necessary that personal interest must make way for a focus on return on investment through graduate outcomes and employability.

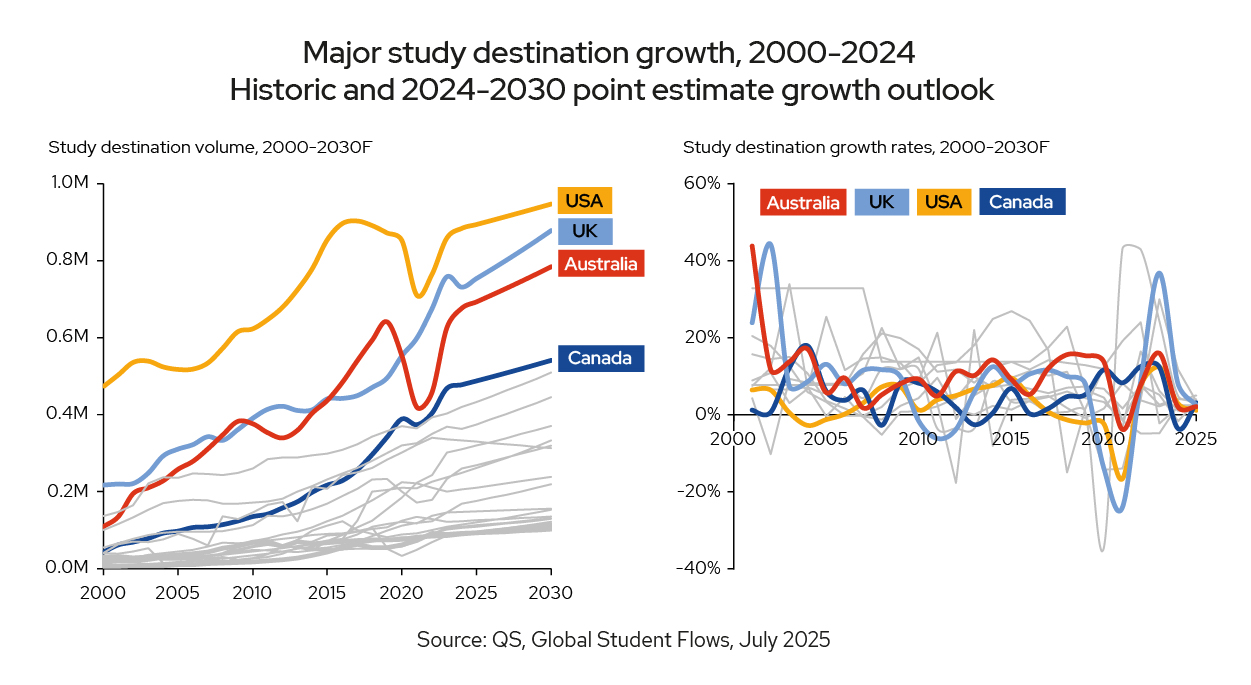

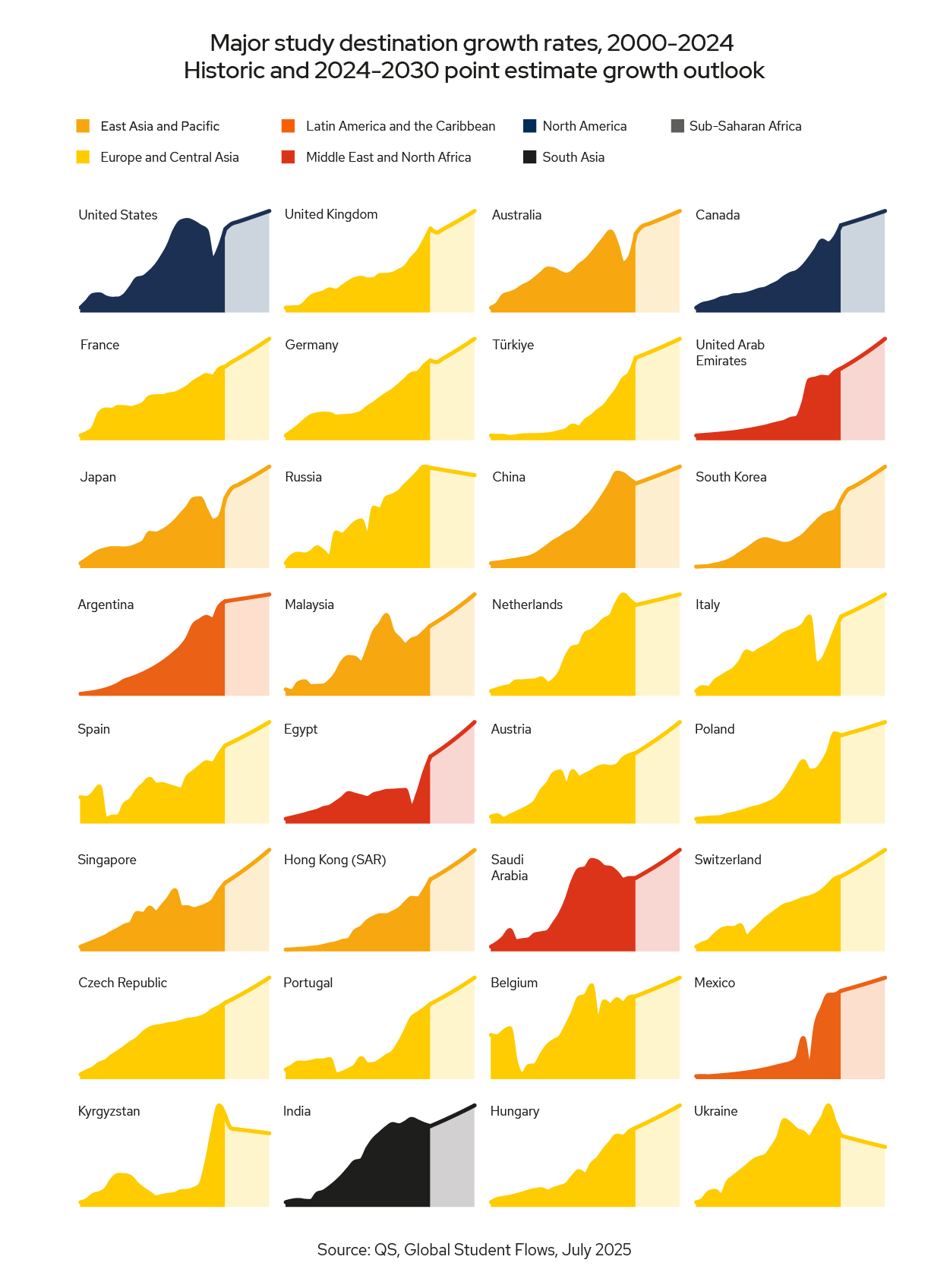

International student mobility is entering a more fragmented, policy-sensitive phase, and it’s no surprise that American policy is once again influencing global student flows. While the US remains the top destination, its leadership in the market is starting to loosen. US international enrolments, excluding Optional Practical Training (OPT), the US post-study work route, peaked in 2016/17 and have yet to fully recover. Although there was a post-COVID bounce starting in 2021/22, total enrolment still trails peak levels by about 2%. Growth has slowed in the last academic cycle, and barring major policy changes, the US is on track for a further slowdown by 2030.

The UK, with post-study work rights restored and a more student-friendly government expected, is the most likely to gain the most among the big four as US growth slows. GSF modelling shows that UK student numbers are projected to approach 900,000 by 2030, up from just over 700,000 today. Australia, despite recent visa tightening and quality control measures, remains attractive for its proximity to Asia and relatively stable regulatory environment. Together with Canada, the top four study destinations are set to retain their status, but their combined market share is forecast to dip to around 35% by 2030, down from 40% a decade ago.

The top 30 destinations collectively host nearly 90% of all international student flows. Looking at projected changes among the top 15 between now and 2030, Türkiye, the UAE, Malaysia, and Japan are each forecast to climb one position, while the Netherlands is projected to drop one rank. Russia sees the most significant shift, falling three places from 7th to 10th. Safety concerns due to the ongoing conflict, along with reputational and logistical challenges, have already prompted a notable decline in student numbers in Russia.

Regions such as the Middle East and Asia are set for strong growth as they compete to become regional education hubs. India, the UAE, Saudi Arabia, Hong Kong (SAR), and South Korea are heavily investing in internationalisation, campus facilities, and English-language programmes. While growth to 2030 in these regions may slow compared to past cycles, it is still expected to outpace the global average. Potential diversification away from traditional study destinations gives them an edge, yet geopolitical instability remains a critical risk for these markets.

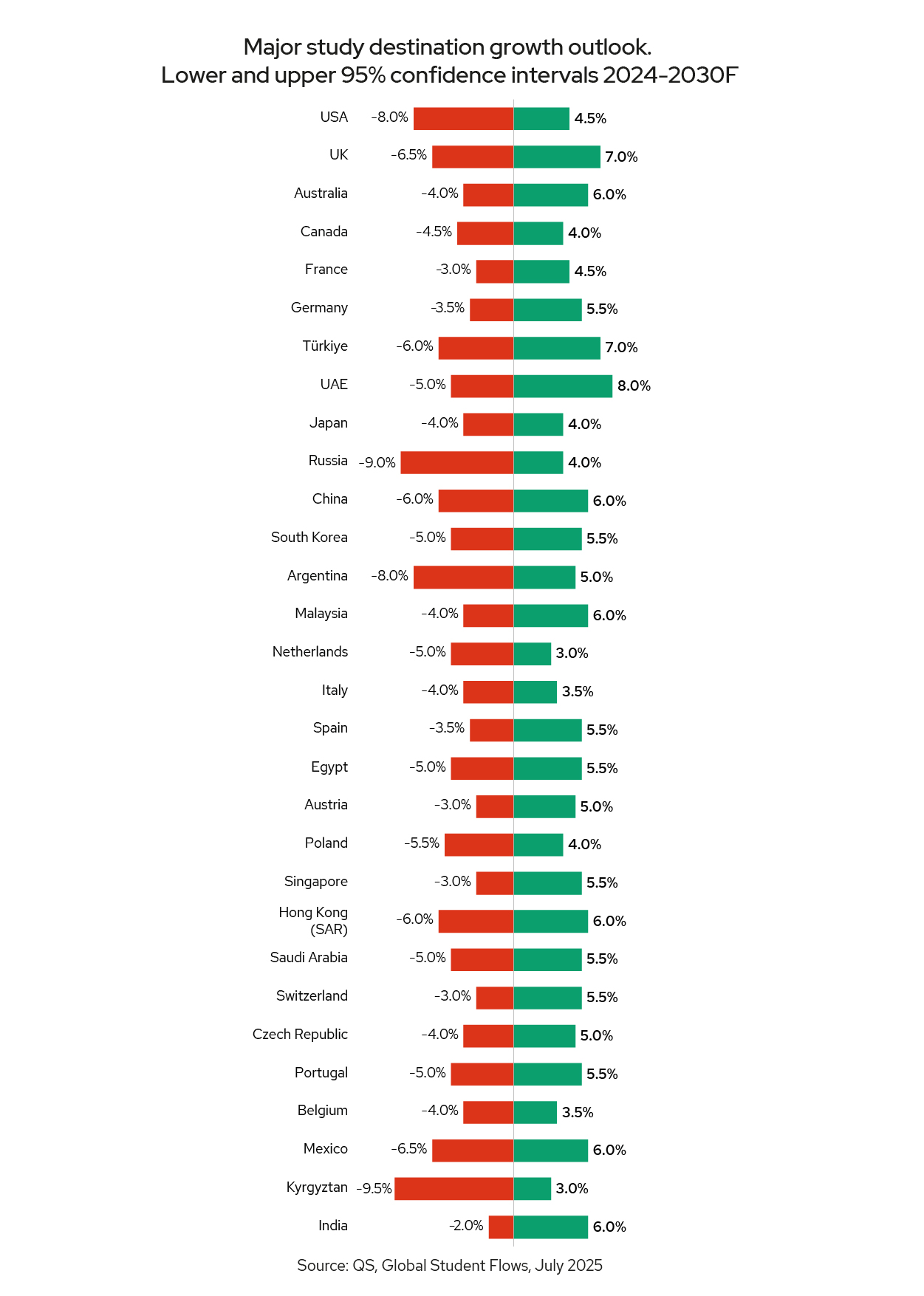

Global Student Flows models the lower and upper 95% confidence intervals in 2030 for international students in every study destination, reflecting how much student growth could vary based on current risks and conditions. A wider spread in the compound annual growth rates (CAGR) indicates greater uncertainty in a destination’s outlook from now until 2030, capturing outlooks from best-case growth to potential headwinds. This is a reflection of how sensitive international students have become to unpredictability in policy and safety concerns.

This spread is notably wide for many nations, reflecting elevated global uncertainty. Major economies like the United States, China and Russia exhibit particularly broad growth confidence intervals as a consequence of their direct exposure to geopolitical uncertainties, and, in Russia’s case, ongoing conflict. Similarly, countries dealing with economic weaknesses or domestic volatility, such as Türkiye, Argentina, and Kyrgyzstan, also show wider confidence intervals. While Türkiye has potential to attract more students from the Eurasia region, the elevated risk environment gives this outlook a slightly negative bias overall.On the other hand, many of Europe’s destinations stand out with narrower confidence intervals, emerging as beneficiaries of the shift away from traditional hubs. These countries combine affordability, accessible visa frameworks, and English-taught programmes, positioning them as stable alternatives. In Asia, Japan and South Korea are set to attract a larger share of Chinese students, fuelled by cooling China-USA relations and strengthening regional academic ties.

However, momentum is set to wane for countries implementing restrictions on student inflows. Canada’s caps have already demonstrably slowed growth, while the Netherlands and Poland, also tightening rules, risk losing their competitive edge. Where immigration is politically sensitive, growth will likely soften. The global student landscape is shifting and fragmenting, with power increasingly dispersing among a broader set of study destinations.

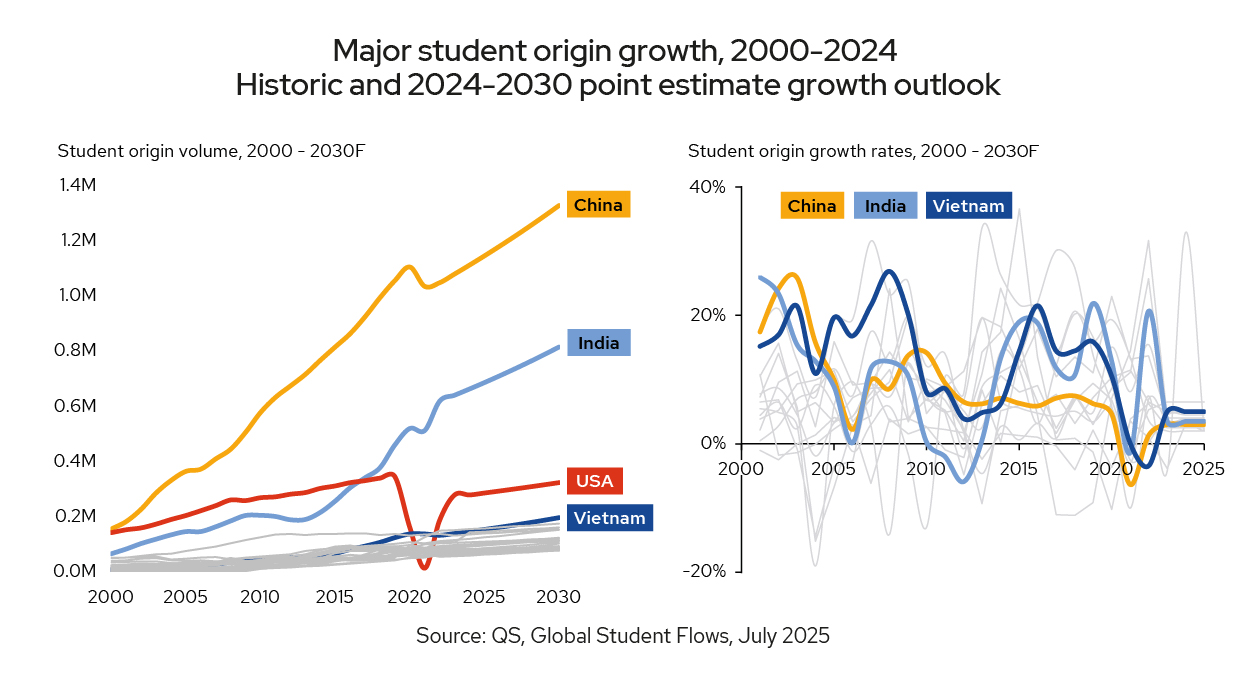

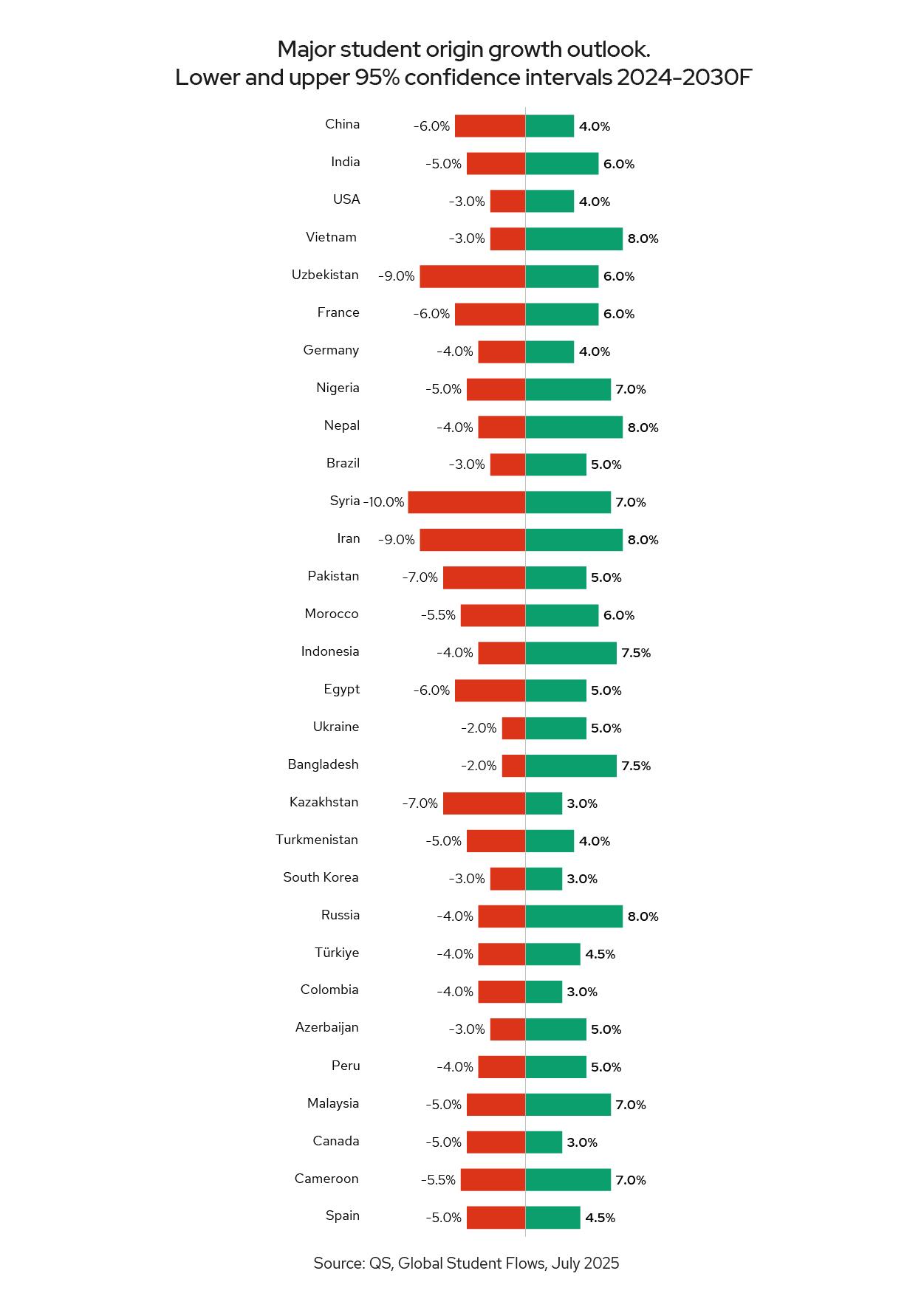

The global supply of international students is set to grow over the next five years, but not evenly. The number of outbound students will be shaped by domestic economic performance, demographics, policy shifts at home and abroad, and geopolitical developments. Countries with rising middle classes and relatively stable economic growth are expected to see increasing outbound student numbers. Vietnam and Indonesia stand out in this regard. Both have young populations, improving income levels, and underdeveloped domestic higher education capacity. They are already among the top 20 source countries, and they are projected to climb further in the ranks by 2030. These students tend to favour destinations like Japan and increasingly Europe, where visa openness and affordability are becoming key attractors.

India is expected to remain one of the top sources of outbound students globally, with an expected long-term annual growth of over 3%. While the Indian government has made it a priority to build up domestic higher education capacity, most notably under the National Education Policy, demand still far exceeds supply, particularly in STEM and post-graduate programmes. India’s population continues to grow and urbanise, fuelling demand for quality education and international credentials. However, outbound growth may slow slightly as Indian institutions scale up and more international branch campuses open within the country.

On the African continent, Cameroon and Morocco are expected to send more students abroad, particularly to destinations that have adopted pro-student policies, such as the UK and France. These countries have scholarship programmes and work pathways with European countries that are likely to boost student flows.

Nigeria has strong potential for outbound student flows. It has one of the most favourable demographic profiles globally, with a fast-growing youth population (23% growth in 18-25 year-olds between now and 2030). However, its persistent economic instability adds a layer of financial risk for outbound students. As a result, while Nigeria is projected to see relatively strong outbound growth in the most likely scenario (4% growth in student numbers), it also has a wider band of possible outcomes. Much depends on how its economy stabilises and whether destination countries continue to offer flexible visas and work policies.

China’s role as a leading sender of international students is facing a slow, structural shift. Economic uncertainty at home, growing cost sensitivity among families, and geopolitical frictions with traditional destination countries - especially the US, Australia, and the UK - are pushing many to look elsewhere or stay within China. In parallel, the Chinese government is investing heavily in domestic universities and promoting local alternatives. While China will remain a major player, its growth trajectory is expected to flatten or slow in this period.

South Korea, meanwhile, is seeing a sharp and steady population decline, with an 8% decline in students aged 18-25 years between now and 2030. This has led to a consistent fall in outbound student numbers, with South Korea seeing outbound declines in all but two years from 2010 to 2022. This pattern is unlikely to reverse in any meaningful way, and South Korea is projected to slip eight spots, falling to 22nd place among source countries by 2030.

Several countries affected by conflict or sanctions - such as Syria, Iraq, and Iran - remain significant sources of international students as well. These students often leave in search of stability, safety, and better opportunities. However, outbound flows from these countries are difficult to forecast reliably. Sanctions, economic collapse, and visa restrictions can rapidly alter the landscape. Iran, for instance, sits at a crossroads with sanctions and domestic pressure pushing students outward, but restrictions can limit how many actually succeed in leaving. For these states, forecasts carry a high degree of uncertainty, with outcomes highly dependent on external policy shifts and internal stability.

Regulated Regionalism describes a scenario in which international education becomes more regionally distributed and governed by formal national frameworks. In this model, major anglophone destinations - such as Canada, Australia, and the UK - implement structured policies to manage international student enrolments through transparent, annually reviewed thresholds and controls. These thresholds are calibrated against factors such as housing availability, institutional support capacity, and national or regional labour market priorities. Institutions are required to demonstrate their ability to support students and deliver programmes aligned with identified skills needs in order to secure allocations.

While demand for international education continues to grow, student mobility becomes increasingly intra-regional. Students from South Asia, West Asia, and Sub-Saharan Africa increasingly opt for high-quality providers within their own regions or in nearby countries. Governments such as India, the United Arab Emirates, Malaysia, Saudi Arabia, and across Central Asia invest heavily in higher education infrastructure, attracting international branch campuses and promoting transnational education partnerships. These developments are supported by the expansion of credit recognition frameworks and multilateral agreements that allow flexible, modular pathways across institutions and borders.

This more distributed model of international education reduces the financial burden on families, shortens travel distances, and offers a hybrid experience - blending regional study with global credentials. For destination governments, it eases pressure on housing and services while ensuring that incoming students are concentrated in sectors of strategic value.

Ultimately, Regulated Regionalism advocates a balanced and managed approach to international mobility - one that retains academic quality and relevance while responding to national capacities and regional opportunity structures.

Hybrid Multiversity envisions a future in which international education is delivered through coordinated, multi-site models that blend online, local, and global learning experiences. In this scenario, many students complete a substantial portion of their degree, often up to half, within their home country or region, either online or through a local partner institution. Shorter, structured periods of study abroad remain a central feature of the experience, focused on activities that benefit most from in-person engagement, such as internships and experiential learning, laboratory work, clinical training, language immersion, and professional networking.

Universities across regions develop common credit-transfer systems, harmonised curricula, and shared quality assurance standards to ensure seamless academic progression. Faculties collaborate across borders to align learning outcomes, assessment schedules, and moderation processes, enabling students to move between delivery sites with minimal disruption. The physical campus is repositioned as a specialised learning environment, prioritising facilities and experiences that cannot be easily replicated online, such as wet labs, design studios, and workplace-integrated learning.

Career development is embedded from the beginning. Micro-credentials earned during the home phase are formally integrated into academic transcripts, providing employers with early visibility of student competencies. Many programmes incorporate remote internships during the early years of study and require in-person placements during the global phase, supporting transitions to graduate employment. Policymakers facilitate this model by simplifying mobility pathways, streamlining visa processes, and recognising hybrid and online components for the purposes of post-study work.

Hybrid Multiversity advocates a more flexible, cost-effective, and coordinated form of international education - anchored in quality and global relevance while responding to evolving student needs, institutional capacity, and labour market expectations.

Talent Race Rebound outlines a scenario in which international education re-emerges as a central mechanism for attracting global talent in response to structural workforce shortages and demographic pressures. By 2030, major destination countries - including the United States, UK, Canada, and Australia - have implemented proactive policy shifts to address skills gaps in fields such as artificial intelligence, cyber and quantum technology, advanced manufacturing, biotech and healthcare and energy and agricultural innovation. Intake caps and administrative constraints that characterised the mid-2020s have been replaced by more efficient, student-centred systems. Visa approvals are processed within weeks, and extended post-study work rights, particularly in high-demand STEM disciplines, are now explicitly linked to structured, points-based migration pathways.

In this context, universities operate in deeper alignment with government and industry. Publicly funded national scholarships target priority fields, while private-sector partners co-invest in graduate internships and offer guaranteed employment outcomes. Research ecosystems are reinvigorated by multi-year public grants, upgrades to research infrastructure, and recruitment of globally recognised faculty, enhancing institutional attractiveness and capability.

Infrastructure constraints, particularly around housing, are addressed through coordinated investment strategies, including public-private partnerships in regional cities. This supports both increased enrolment and a more balanced geographic distribution of students.

For international learners, the proposition is compelling: a full-degree, on-campus experience that offers access to world-class academic environments, robust professional networks, and a credible path to long-term employment and residency. Families increasingly view the investment as a gateway to opportunity, and application volumes from larger emerging markets - such as India, Nigeria, Indonesia, and Brazil - rise sharply. International education, once primarily seen through the lens of cultural diplomacy, is now a key strategic lever in the global competition for human capital.