.jpeg)

Global Student Flows | United States

17 February 2026

International education remains a cornerstone of US global influence, but shifting geopolitics, policy uncertainty, and changing student demand are reshaping the country’s role in global mobility. The QS Global Student Flows: United States report examines projected enrollment contraction through 2030, emerging growth markets, and the rising importance of diversification, employability, and skills-based education. Drawing on evidence-based modelling, it explores inbound and outbound flows, competitive pressures, and strategic scenarios to help institutions adapt and thrive in a changing global landscape.

Get a snapshot of the insights below. Download the PDF for the full report.

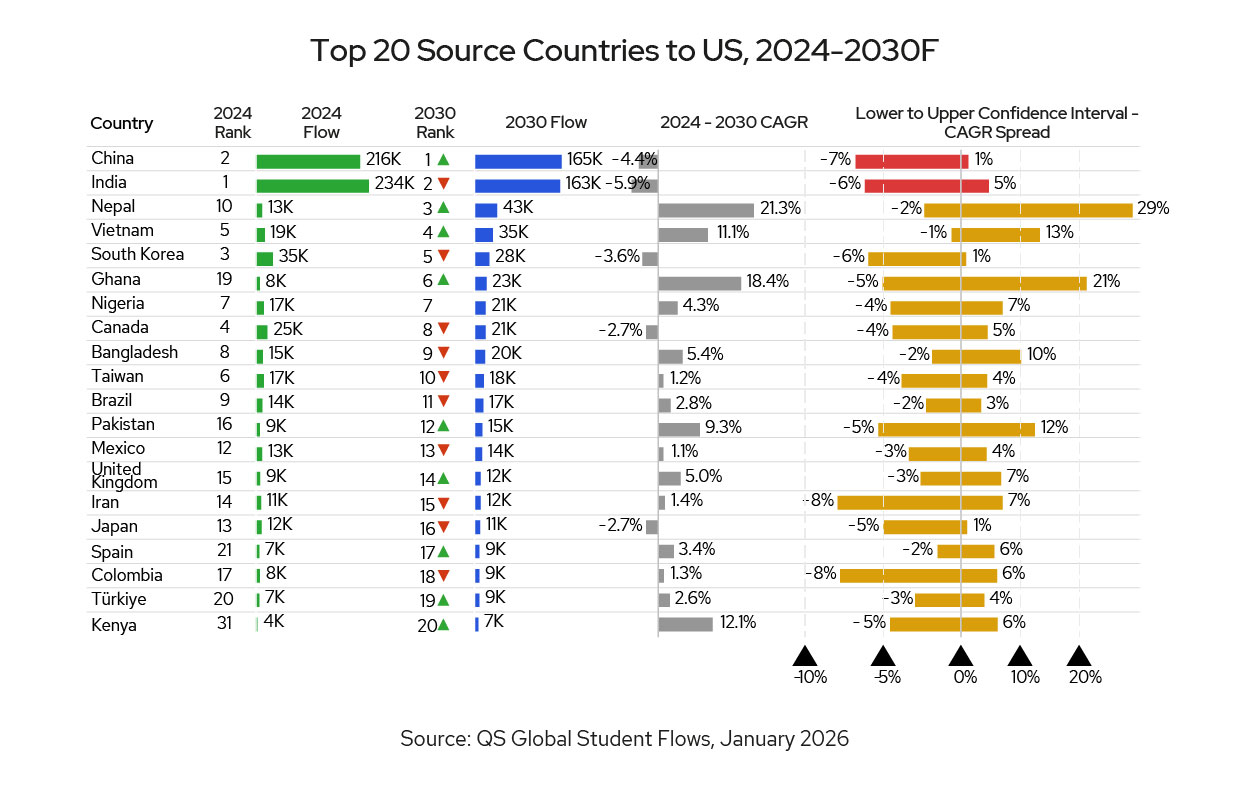

The United States remains a leading destination for international students, but faces a period of mild contraction in enrollments, projected to decline by approximately 1% annually through 2030. This trend follows years of stagnation, with recent data showing flat or negative growth, especially when excluding Optional Practical Training (OPT) figures. The forecast contraction is driven by geopolitical shifts, changing visa regimes, labor-market incentives, and cost and demographic pressures. Major source countries such as India, China, and South Korea are sending fewer students, with India’s numbers particularly vulnerable to changes in work-rights policies and visa uncertainty, and China’s decline is seen as an enduring trend due to structural and political factors.

Despite these challenges, there are bright spots: Africa is poised for strong growth, led by Nigeria and Ghana, while smaller markets like Nepal, Bangladesh and Vietnam show resilience and above average growth.

This forecast contraction, and dependency on the policy environment through 2030, underscores the need for scenario-based planning. Our three scenarios - Regulated Regionalism, Hybrid Multiversity, and Talent Race Rebound - each highlight the need for strategic adaptation, diversification, and closer alignment with labor-market needs.

Outbound US student mobility is rebounding, with increasing numbers studying abroad, especially in Mexico and the UK. Transnational education and online/hybrid programs are expanding, offering new pathways for global engagement.

As the number of international students choosing the US stagnates, US institutions will remain in a battle for existing market share. To remain competitive, US institutions must enhance their value proposition, focusing on employment outcomes. International students increasingly seek return on their investment through job opportunities and post-study work.

Overall, the next decade will demand that US institutions engage in deliberate diversification, proactive engagement with policymakers, and a commitment to flexible, skills-based education.

US institutions face declining numbers from major markets such as India, China, and South Korea. The challenge is to diversify recruitment pipelines and capture growth from emerging regions.

With increasing competition and rising costs, colleges must reverse diminishing reputation among employers, and focus their messaging around academic excellence and employment outcomes. Demonstrating clear return on investment is crucial.

Rapidly changing labor-market needs, especially in STEM, healthcare, and advanced technologies, require institutions to adapt curricula and support services.

Shifting visa regimes, OPT policies, and global competition create uncertainty for students and institutions. US institutions must remain agile, engage proactively with policymakers, and communicate clearly about work rights and post-study opportunities.

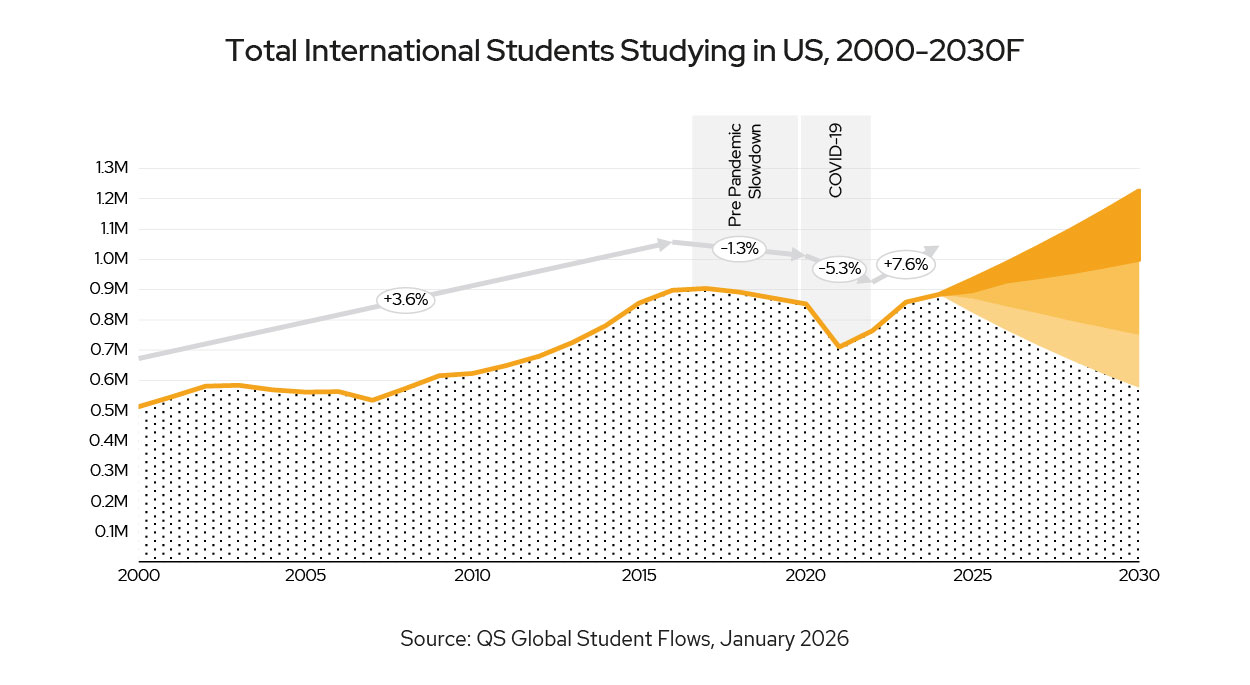

International student enrollments in the United States are entering a period of mild contraction, with total numbers projected to decline by roughly 1% annually through 2030. For context, US inflows grew by only 0.2% each year in the six years leading up to 2025, following a 3% annual growth rate recorded in the six years prior. In terms of the outlook, the headline figures mask a more complex reshaping of global demand, driven less by academic considerations and more by geopolitics, visa regimes, labor-market incentives, and demographic pressures. For US universities, the next five years will be defined by tighter competition for talent, heightened sensitivity to policy signals, and shifting opportunities across fast-growing but volatile emerging markets.

The latest Open Doors release illustrates the underlying deceleration. While total enrollments (including OPT) grew by 4%, enrollments excluding OPT - a more accurate reflection of actual student inflows - fell by 0.1%, essentially flat. For comparability, the QS Global Student Flows model removes OPT from the US figures, aligning them with how other countries report enrollments. The stagnation was driven by contractions from major Asian markets; India, China, and South Korea collectively sent nearly 30,000 fewer students than a year earlier. When OPT is included, India appears to have grown (+9%), yet this masks a decline in new academic enrollments and underscores the fragility of US-bound demand once post-study work opportunities are excluded from the narrative.

Data from IIE’s 2026 snapshot further confirms this softening. Total enrollments, including OPT, declined by 1% in 2026 according to the data. Undergraduate (+2%) and OPT (+14%) numbers remain resilient, but postgraduate levels fell sharply (-12%), an early warning sign as PG programs typically anchor long-term growth and research capacity. The 17% drop in new enrollments in 2026 signals that by 2027 there is likely to be a significant contraction in overall enrollments from current levels, likely in the mid-single-digit range. Our projections suggest that the downturn in overall enrollments will bottom out before modest recovery resumes toward the end of the decade, averaging to approximately a 1% annual decline in total enrollments from now through 2030.

Geopolitics and immigration policy will set the tone. India - long one of the engines of US international enrollment growth - is expected to decline by around 7% through 2030. A decisive factor is the country’s heavy reliance on OPT; over 30% of Indian students in the US are on OPT pathways. While OPT is excluded from the Global Student Flows model, it remains central to student decision-making. Any tightening of work-rights policies, uncertainty around future visa rules, or competition from destinations offering clearer post-study routes risks further weakening India’s inbound pipeline. Rising concerns about affordability, stricter US consular reviews, and long visa appointment backlogs also weigh on sentiment.

China, meanwhile, faces structural rather than cyclical pressures. The US–China relationship remains fraught, and while economic interdependence tempers the downside, persistent security concerns, restrictions on sensitive fields, and political rhetoric have prompted families to diversify study destinations. The US is still viewed favorably for STEM excellence, but China’s outbound mobility has plateaued. We project a continuation of the roughly 4% annual declines seen in recent years. Domestic factors - slower economic growth and Beijing’s push to strengthen its own higher-education system - further dampen outbound flows. For US institutions, China’s retreat is likely durable rather than temporary in contrast to the decline in India’s numbers which are likely to rebound.

South Korea’s decline is more demographic than geopolitical. The country’s shrinking youth population has reduced overseas study volumes for more than a decade, and this structural trend will continue into the 2030s. While the US remains a preferred destination, the total pool of outbound students is simply smaller each year, leaving limited room for reversal.

There are, however, bright spots. Africa is poised to deliver the strongest regional growth, led by Nigeria and Ghana, where demographic momentum and demand for high-quality education remain robust despite economic headwinds. Visa policy will be decisive; improved processing consistency and targeted recruitment could convert latent demand into sustained inflows.

South Asia - which was the fastest-growing region in the 6 years to 2024 - is expected to contract by around 2% over the next six years, largely because India constitutes such a large share of US-bound traffic. Yet within the region, smaller markets such as Nepal and Bangladesh continue to show surprising resilience and are likely to maintain double-digit growth.

Vietnam also stands out as an emerging engine of growth, posting an 18% increase last year. Its expanding middle class, strong English-language preparation, and preference for business and STEM fields position it as one of the most reliable medium-term markets for US institutions.

Overall, the coming decade will demand more deliberate diversification, tighter alignment with labor-market narratives, and proactive engagement with policymakers. The US remains a top global destination - but will need to work harder to stay there.

Under a Regulated Regionalism trajectory, international student mobility becomes more regionally distributed, and the United States faces a more competitive, policy-structured global environment. While US demand remains strong, a growing number of students - particularly from South Asia, East Asia, the Middle East, and Africa - pursue high-quality regional alternatives due to geopolitics, rising investment in local universities, branch campuses, and transnational digital pathways. This reduces the proportion of globally mobile students who automatically view the US as the default destination.

In parallel, Canada, Australia, and the UK increasingly formalize international student intake thresholds based on housing supply, institutional capacity, and labor-market alignment. Although the US does not move toward national quotas, federal agencies and state systems adopt tighter monitoring frameworks: requiring clearer evidence of institutional support capacity, improved transparency on employment outcomes, and enhanced oversight of student services.

To encourage inbound flows, US universities respond by sharpening their value proposition - highlighting research-intensive environments, industry linkages, and disciplined student-support structures. Competition intensifies for applicants in priority fields such as computing, engineering, and health sciences, while overall mobility becomes more selective and program-specific.

Regionally concentrated flows elsewhere mean the US receives a smaller share of students seeking lower-cost or shorter-distance study. Under Regulated Regionalism, the US international student market attracts those prioritizing advanced research, reputation, and post-graduate opportunities.

The Hybrid Multiversity scenario envisions a US international education system increasingly embedded in multi-site, digitally enabled learning models. By 2030, a substantial share of prospective students engage with US institutions through partnerships in their home countries - completing foundational coursework online or through local affiliates before undertaking shorter, targeted study phases in the United States.

These US-led hybrid pathways are supported by expanded credit-transfer agreements, jointly delivered curricula, and shared quality assurance arrangements with institutions abroad. Faculty collaboration tools allow alignment of syllabi, assessment calendars, and moderation systems, enabling smoother progression into US campuses.

On campus, the US learning environment evolves toward specialized, high-value experiences: research labs, clinical and engineering training sites, entrepreneurial incubators, and applied industry partnerships. Students visit the US for periods that maximize hands-on learning, professional networking, and workplace-integrated internships.

Career development becomes embedded into the model. Micro-credentials earned during the home-country phase - often tied to digital skills, analytics, or professional competencies - are integrated into US academic records. Universities work with employers to structure hybrid internships, including remote placements early on and in-person capstone experiences in the US.

Policymakers streamline visa processes for short-term academic mobility and clarify how hybrid or online components count toward work authorization and practical training pathways. These adjustments maintain the US as a central anchor in the global learning ecosystem while making study abroad more flexible and cost-efficient.

The result is a diversified US international education model; globally connected, digitally supported, and oriented toward high-impact learning and employability outcomes.

In the Talent Race Rebound scenario, international education becomes tightly linked to the United States’ efforts to address structural workforce shortages and maintain competitiveness in advanced technology sectors. By 2030, demographic pressures and rising demand for specialized skills push federal policymakers to prioritize international talent attraction as part of a broader economic strategy.

US agencies streamline visa processing for students in priority fields such as artificial intelligence, cybersecurity, quantum science, advanced manufacturing, health professions, and clean energy. Processing times accelerate, compliance systems become more efficient, and pathways from study to work - particularly through OPT and STEM OPT - are clarified and expanded. Discussion around structured, points-based transitions to employment gains momentum in high-demand sectors.

Universities operate in closer alignment with industry and government. Public and private scholarship schemes grow, targeted at programs with clear workforce relevance. Employers co-invest in research partnerships and graduate internships, creating more predictable pipelines from study to skilled employment.

Research ecosystems benefit from federal investments in laboratory infrastructure, regional innovation hubs, and globally competitive faculty recruitment. These factors enhance institutional attractiveness for international students seeking research-intensive environments.

Housing and capacity constraints are addressed through coordinated public–private development in campus-adjacent and regional innovation districts, enabling institutions to scale enrollment sustainably.

For students, the US offers a compelling combination; world-class academic environments, technology-driven research opportunities, and credible post-study employment pathways. Large emerging markets- particularly India, Nigeria, Indonesia, and Brazil - respond strongly, driving increased applications to STEM and health programs.

In this scenario, international education consolidates its role as a strategic lever in strengthening the US workforce and innovation system.

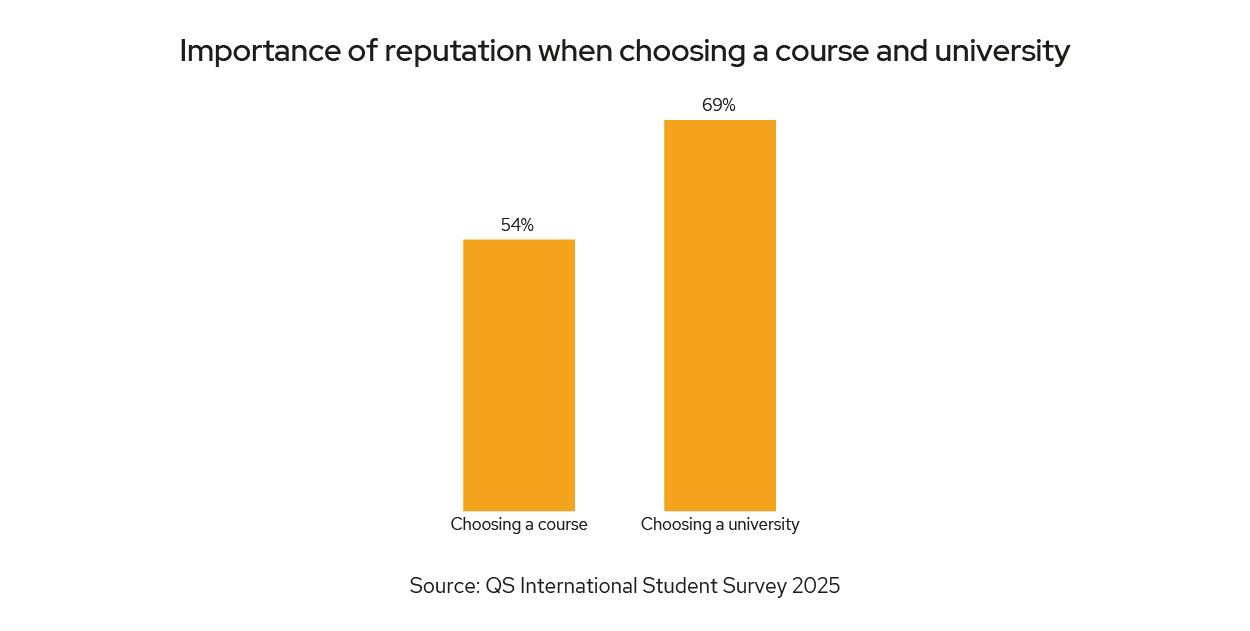

Those looking to study in the US are largely driven by reputation. When choosing a course and university, 54% and 69% of students respectively said reputation was important (Figure 15). However, data from the QS World University Rankings shows that work must be done to retain Academic and Employer Reputation. Since 2017, the Median Academic and Employer Reputation rank of US colleges has declined (Figure 16 and 17).

In the face of increasing tuition and living costs, maintaining a solid reputation – which many students associate with performance in university rankings – will be critical for students to justify their investment.

.jpg)

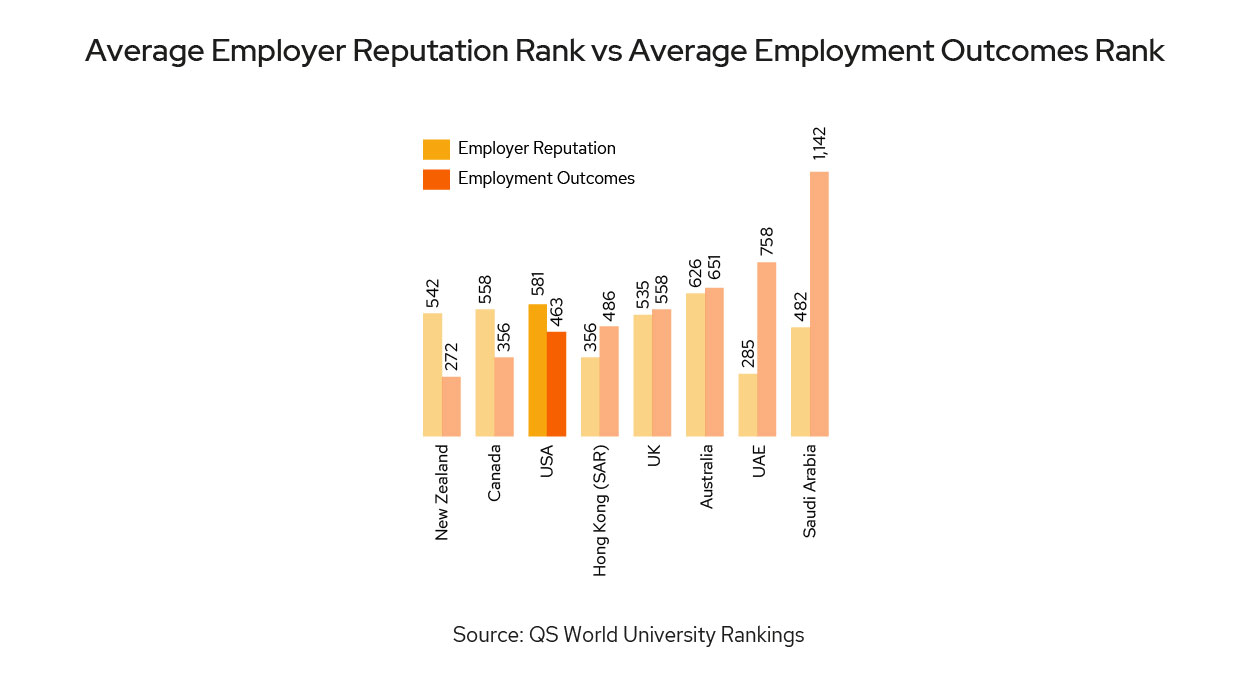

Another way US universities can show return on investment is through their Employment Outcomes. As explored earlier, OPT is a major driver of highly skilled students studying, and working, in the US. This is unsurprising, as we see the average Employment Outcomes rank is lower, and therefore better, than the average Employer Reputation rank (Figure 18). Clearly, US universities and colleges are able to deliver positive graduate outcomes, with graduates securing jobs at high rates, and nurture alumni that go on to make an impact on society. However, US institutions’ average reputation among employers is lower than these strong graduate outcomes would suggest. Leveraging the successful narratives of graduates will be critical to reversing the decline in US Employer Reputation.

While the median Employer Reputation rank has declined, post-study employment prospects remain crucial in student decision-making. Overall, 50% of all students looking to study in the US report that information on work placements and links to industry are useful in marketing communications (Figure 20); in the key source markets of South and East Asia, that number rises above 50% (Figure 20).

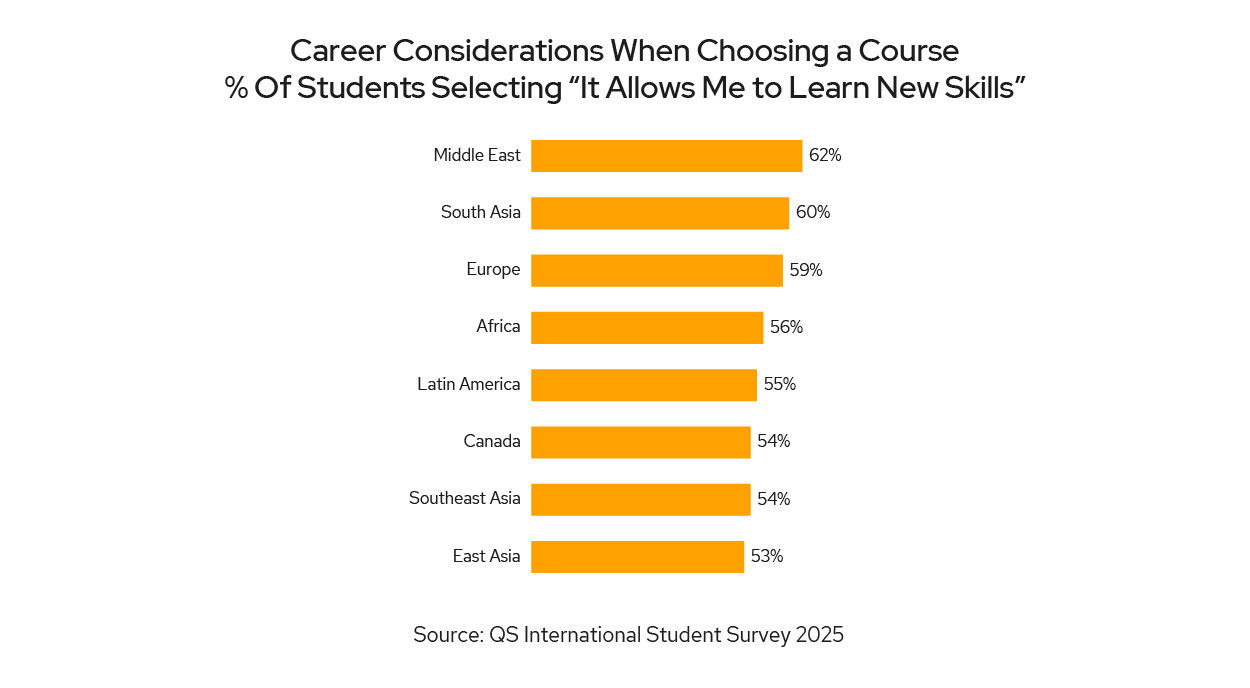

Regardless of region, a majority of students say that, when thinking about career considerations while choosing a course, they base their decision on whether the program allows them to learn new skills (Figure 19). This further emphasizes the importance of skills-based curricula, and using employability as a lever to recruit new students. Students view their college experience as the ideal opportunity to upskill and to learn how to articulate the value they can add to prospective employers through the skills they acquire.

US institutions must broaden their recruitment strategies beyond traditional markets - India, China, South Korea – and tap into emerging regions such as Africa, Southeast Asia, and resilient smaller markets like Nepal, Bangladesh, and Vietnam. This diversification will help offset declines in major source countries and capture new growth opportunities.

Institutions must proactively align curricula and support services with labor-market trends, especially in high-demand sectors like STEM, healthcare, and advanced technologies. Partnerships with industry and government, as well as expanded work-based learning opportunities, will be essential for demonstrating employability and supporting student career ambitions.

Colleges must sharpen their messaging around academic excellence, research opportunities, and employment outcomes. Highlighting successful graduate stories and leveraging strong alumni outcomes will be key to reversing declines in median Academic and Employer Reputation rank, and attracting students who are increasingly focused on return on investment.

Institutions must proactively align curricula and support services with labor-market trends, especially in high-demand sectors like STEM, healthcare, and advanced technologies. Partnerships with industry and government, as well as expanded work-based learning opportunities, will be essential for demonstrating employability and supporting student career ambitions.

US universities need to remain agile in response to changing visa regimes, OPT policies, and global competition. Proactive engagement with policymakers and clear communication about work rights and post-study opportunities will help maintain the nation’s attractiveness.